So, in a bank’s balance sheet, the loan is shown as accounts receivable (amount that will be received in the future) on the assets side.

But, what if the bank wants to realize this amount before the scheduled period of 30 years?

What if the bank wants the entire outstanding amount today? Can they get it?

YES, by a process called securitisation.

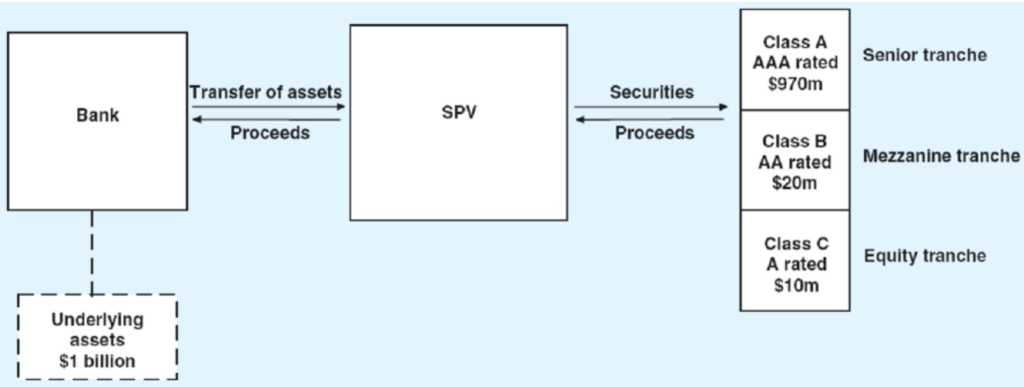

Banks can transfer the entire loan amount to an entity which is a special purpose vehicle (SPV). SPV is a legal entity used by banks to isolate them from the financial risk (risk that involves financial loss to the bank i.e. if the borrower doesn’t repay the loan).

Simply said, banks transfer the assets (accounts receivable in this case) to the SPV. In return, the SPV will give the present value of all the components to the bank on the day transfer of such assets. If the total of all components is US $1 billion, then the present value of US $1 billion [Present value = Future value/ (1+rate) ^ no. of periods] will be given to the bank as proceeds. The EMI which is due from the borrowers will now directly go to the SPV (and not to the bank anymore).

Have a look at the image attached below:

{kind=link}