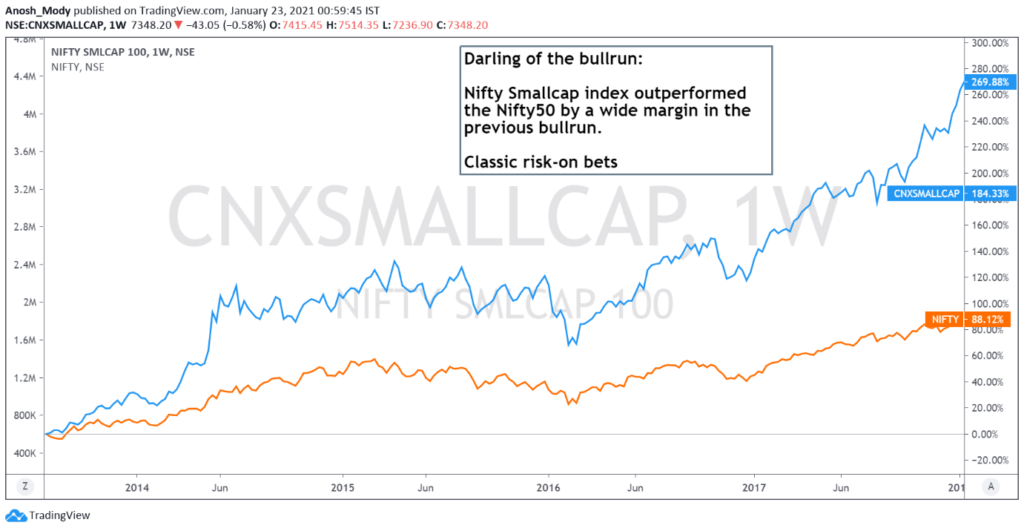

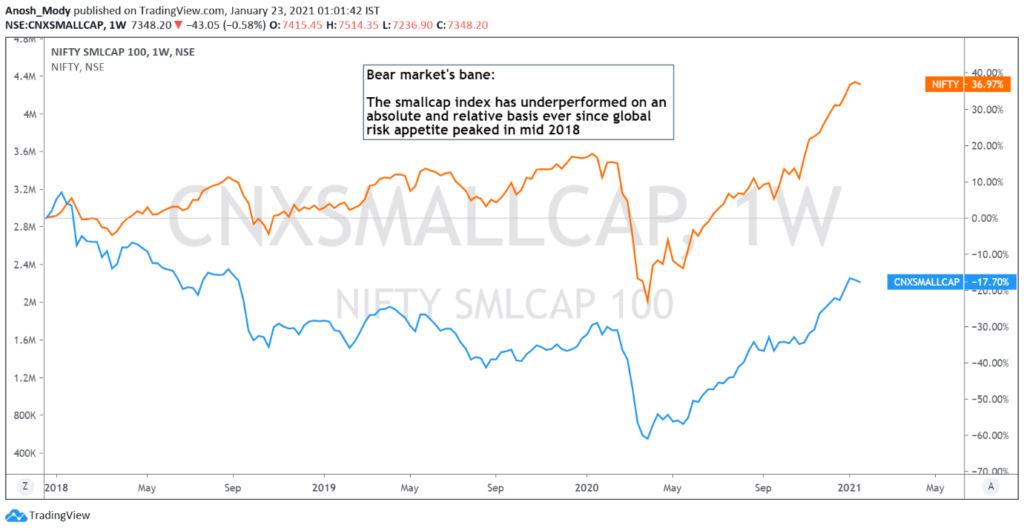

We see how participating aggressively in smallcaps in the bull-run of 2013-2018 was wildly profitable, and led to disproportionate gains for risk loving investors. At the same time, we see how the smallcap index has still not managed to recover from the correction after its 2018 peak, which means a lot of investors are probably still stuck with stocks that they bought in euphoria, and were unable to sell, even though the Nifty50 went on to make new highs over the next 3 years.

Hence, it is important to identify what part of the market cycle we are in, while making smallcap investing decisions.

That’s the when, now let’s talk about the WHAT. Smallcap investing requires strict fundamental filters. I believe in buying growth at reasonable valuations, after carefully analysing the key growth drivers, while trying capitalise on large macro trends. Companies should be filtered out based on visibility of earnings, ability to generate free cashflow, low leverage, sustainable return ratios and last but not the least, management quality and corporate governance.

Despite all of this, there are a few issues that deal smallcap investing a bad name:

The shares of smallcap companies are often illiquid, with very shallow trading volumes. This makes them easy targets for price manipulation, and can adversely affect serious long-term investors, as the share price in the short run can be incredibly volatile.

There are quotes that one often reads in financial media, such as: “If you had invested Rs. 1 lakh in Havells in 1996, it would be worth more than Rs. xx crores today!” Well, they forget to add the assumption: “assuming you didn’t cash out at 5, 10, 15 or even 100 lakhs”. In reality, holding on to a winner long enough, and allowing it to compound over years is not easy.

Expecting a smallcap portfolio to perform like a largecap one by consistently beating a benchmark is a naïve habit, and more often than not, leads to investors selling their diamonds while they are still in coal form. Value unlocking takes time, and that is something every smallcap investor must come to terms with before venturing into this territory.

The path for smallcaps going forward, from a technical viewpoint:

The charts below show that the smallcap index is considerably away from its All Time High, while the relative strength chart with the Nifty50 is ready to breakout from an inverted head and shoulders pattern. This means that going froward, we are likely to see a period of serious outperformance by smallcaps, similar to what we saw in the golden period for stock markets, i.e., late 2013 to early 2018, when the smallcap index nearly tripled.

{kind=link}

Thanks Anoosh. as always, a pleasure to read