In today’s #Tfpforall we try and simply the terms Mortgage and Moratorium for you guys!

Mortgage

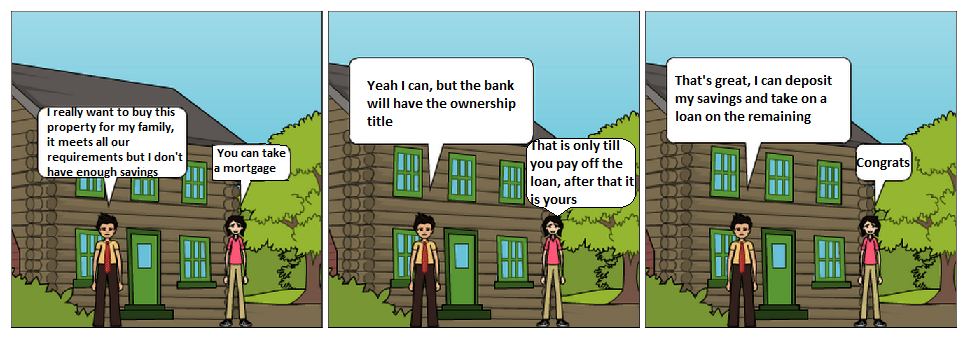

Suppose there is a house you have been eyeing, it perfectly matches your dream house. The only problem is that it costs Rs. 10 lakhs and you have only Rs. 2 lakhs saved, approximately 20% of the price. So you go to a bank and ask for a loan on the remaining 80%. The bank after verifying your credibility, agrees to pay Rs. 8 lakhs on your behalf to the seller of the house on the condition that while you are paying off the loan (either through monthly or yearly installments), bank will have the title of the house. This means the title of the house goes to the bank to “secure the loan”. This securing of loan is technically what constitutes a mortgage. Mortgage is a debt instrument backed by a particular real estate property. Mortgages are used by individuals and corporations to buy huge real estate properties without having to pay the whole amount upfront.

Moratorium

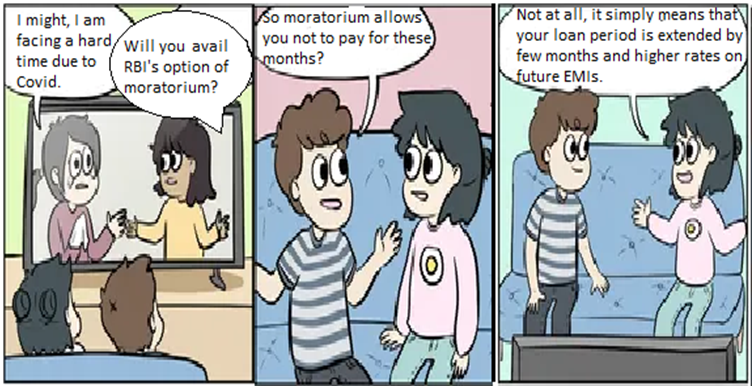

With RBI recently extending the moratorium for another 3 months, let’s understand what moratorium really is. Moratorium is basically legal suspension of an activity by government or a company, due to temporary financial hardships, like natural calamities. It’s often in response to financial turmoil that projects inability of borrowers to pay interest, just like how the current Coronavirus pandemic has created a disruption in our usual lives. A moratorium period on terms loan means a time period during which the borrower does not need to make any repayment.But that doesn’t mean, your interests of these three months is forgotten or postponed, it simply means that your interest rates will continue to accrue even on the deferred amount, which will either be paid in lump sum or will be spread over future payments, that will effectively increase the future loan EMI. So should you avail this option? It totally depends on availability of cash with you. If you are facing liquidity crunch and can’t afford to pay EMI, definitely go ahead. In fact, a survey reported that one out of three borrowers availed this option. But also keep in mind the risks attached of longer tenure, which will also mean higher future cost.