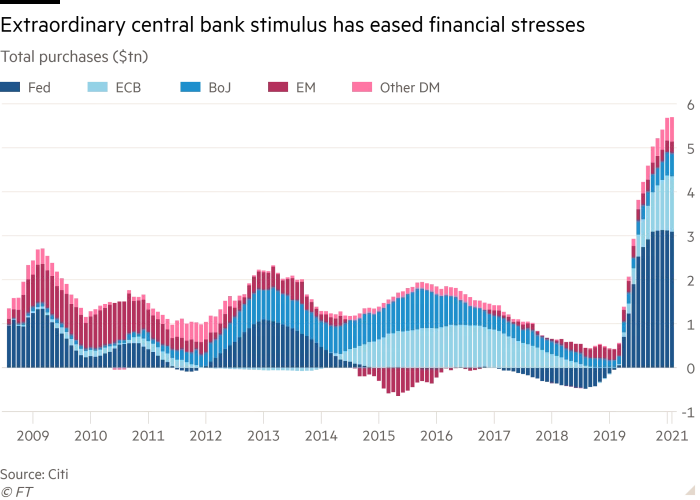

This Fed again overstepped by injecting trillions of dollars of bailout money in the form of grants with some strings attached (such as limits on executive compensation or stock buybacks) and loans. The ultimate purpose of these bailouts is to keep capital flowing, as the Covid-19 outbreak prompted a massive, indeterminate economic shutdown via nation-wide lockdowns.

What’s different from the Troubled Asset Relief Program (TARP) bailout of 2008 is that, unlike the banks and financial institutions whose negligence caused the mortgage collapse, the airlines’ and many other industries’ predicament wasn’t of their own making.

The U.S. government’s buying up of the private sector’s junk-bonds, which is beyond what has ever been done, even in the 2008 financial crisis, is arguably distorting asset values in the process. The vast expansion of the Fed’s activities in funding the private sector, in particular, it’s purchase of corporate debt, has led to more capital within corporations who have used this spare cash for stock buy-backs, increasing dividends for a smaller pool of investors, as well as massively inflating the price of their company stock. The Fed does this by buying up corporate bonds, which includes below-investment-grade credits (speculative class bonds), more popularly named; junk bonds.

The purchase of speculative classes, means passively investing in credits, by the Fed has caused the greatest outburst in the capital markets. The selective capital allocation of the Fed can either be looked at prudent investment or plain nepotism. In the ETF basket, the biggest debtors get the largest weight, and concurrently some of the worst credits also get lumped into the basket. Conclusively, the Fed is using public money to assist dicey debtors, such as the US shale industry.

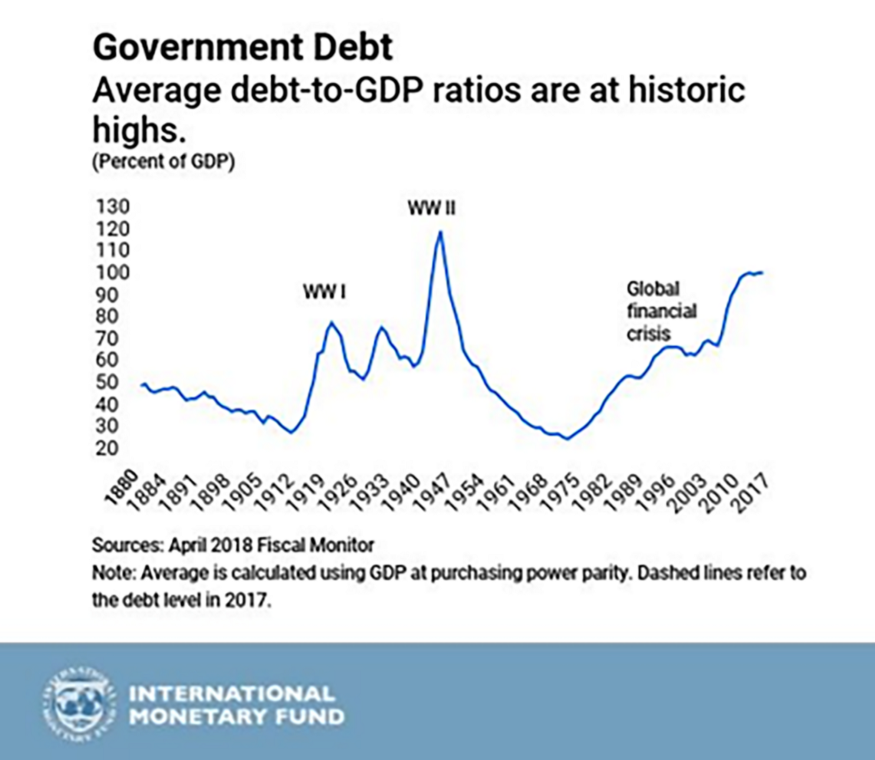

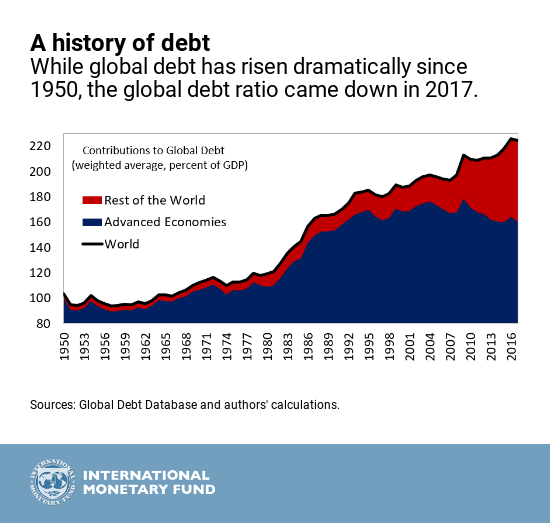

Ultimately, this has led to deferring the loan cycles of an existing over-leveraged economy. Resulting in the ballooning of the liability sides of the balance sheet — eventually directing us back to an even more slippery Global Debt Crisis. This is because, for a balance sheet to balance, assets must be equal to liabilities. But not just the US but the global economy has been constrained by more debt, there is more debt than assets. For the debt-led system to work, you need to make money from debt. However, it seems that we are now creating more debt from debt, perpetuating the crisis.

{kind=link}