What if I tell you that there’s an investment product which can give you all the upside of Equity while protecting or almost no downside?

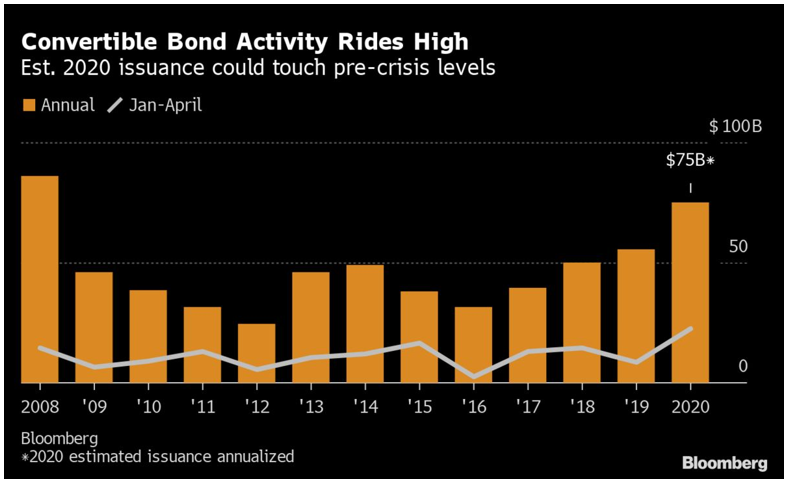

These are very rare and scarce instruments called Convertible Bonds. (Preferred Bonds and Warrants are also somewhat similar instruments as well)

Convertible Bonds are not just one more boring fixed-income instrument, they are corporate debt securities that yield interest but can be converted into a per-determined number of Equity Shares.

Conversion on the bond can only be done when the company opens the window but the decision lies in the hands of the investor.

The yield on the bond is subject to underlying stock price and the credit rating of the company. Usually, the yield is lower than that of traditional bonds as the investor gets the privilege of conversion and priority during repayment. A Zero Yield Convertible Bond can be considered as buying long term Call option without worrying about the premium decaying as the upside is unlimited if converted at a good rate.

If the stock goes down the investor has the right to be repaid the principal and interest, if they succeed and the stock goes up they can convert it into shares.

{kind=link}