Affle India is one of the most scalable, asset-light, and profitable digital businesses listed on the Indian stock exchange today. Affle is a global technology company with a proprietary consumer intelligence platform that delivers consumer engagement, acquisitions, and transactions through mobile advertising.

Affle India was founded by two Anujs – Anuj Khanna Sohum and Anuj Kumar. Together, they listed Affle in 2019, which was oversubscribed by 86 times, a record for an internet company at that time. The issue price was set at 740 – 745. And as of 6th June 2021, the share price is 5,349. An astonishing seven-fold multiplication in share price.

Affle also stepped up their acquisition game as of late. They acquired two companies in 2020, appnext (mobile app discovery and recommendation) and MediaSmart (European mobile programmatic & proximity marketing). In the last three years, the company has gone ahead with five acquisitions which have helped them to build ground in various aspects from digital ad fraud detection to simplifying the omnichannel business. On 10th June 2021, the company announced that they’d acquire Jampp, a mobile marketing firm based in Latin America.

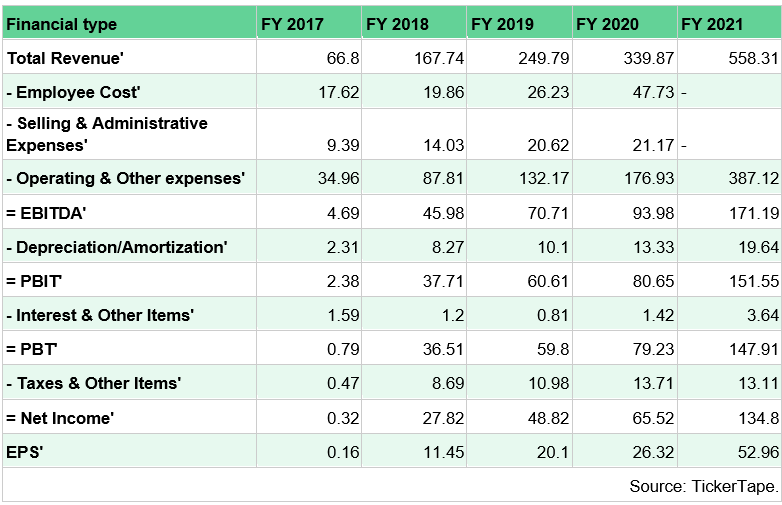

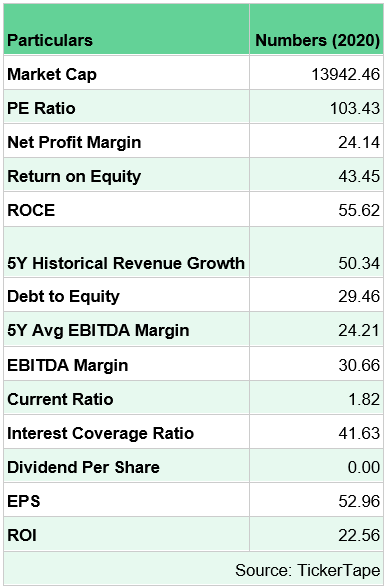

Affle’s business model is very asset-light, and the company also has good investors such as Microsoft, Bennett Coleman & Co., Centurion corp, D2C, and Itochu. The FII holding of the stock has also gone up from 8.37% in Sept 2020 to 19.87% in May 2021. This increase is because the business model has leaps of growth ahead of it. The business functions with good margins of the net profit margin of 24.14%, making it a very attractive company.

Affle focuses on two business segments –

I. Consumer Platform

II. Enterprise Platform

Consumer Platform:

The consumer platform delivers consumer acquisitions, engagements, and transactions through relevant advertising for leading B2C companies. The consumer platform provides the following services –

1. New Consumer conversions (acquisitions, engagements, and transactions)

2. Retargeting of consumers to close their transactions

3. Online to offline platforms that convert online consumer engagement into meaningful in-store walk-ins.

Enterprise Platforms:

Provide end-to-end solutions for companies to enhance their engagement with mobile users by developing apps, provide enterprise-grade analytics for more engagement.

The consumer platform contributes to 97.2% (2020) of the company’s revenues; meanwhile, the enterprise business only contributes to only 2.8% of the revenues. However, both the segments are growing in leaps and bounds; in 2019-2020, the consumer platform revenues grew, 34.1%, and the enterprise business grew 23.8% Y-O-Y.

{kind=link}