The unprecedented crisis has shown us the phenomenal growth IT industry has brought to the forefront, solidifying India’s importance as a knowledge powerhouse. But this competitiveness is restricted to the services sector by and large. In fact, this sector is contributing to the overall GDP, exports and a destination for Foreign Direct Investments (FDIs) in the country. Despite showing a good growth performance over the last few years, the manufacturing sector is still behind the service sector although three industries constituting the growth are pharmaceuticals, auto parts and cotton textiles. Though these sectors are showing much dynamism in exports. India’s exports have now diversified to encompass services.

The growth of R&D outsourcing is an illustration of the country’s prowess in high technology activities. An interesting dimension of high technology production in India is that this capability rests purely in services. This indications that the capability in high tech services is slowly percolating to high tech manufacturing now. The sector where it is very clearly visible is in the area of telecommunication where a revolution of sorts is taking place.

How Telecommunications is contributing to the growth

India ranks as the world’s second largest in terms of telecommunications market with a subscriber base of 1.6 billion. India is one of the biggest consumers of data worldwide. And the number of internet subscribers increased at a CAGR of 21.36% in FY16 to reach 734.19 million in FY20. It has been a critical economic multiplier that cuts across all sections of the society and amongst the most competitive and challenging businesses in the economy.

The gross revenue of the telecom sector stood at Rs. 66,858 Crs. (US$ 9.09 billion) in the first quarter of FY21. No other sector has clocked such a high rate of growth. Robust policy support from the Government has been crucial to the development of the telecom. The increase in Foreign Direct Investment (FDI) cap in the telecom sector from 74% to 100% has brought an FDI inflow of US$ 37.27 billion during April 2000-June 2020.

The story so far

Liberalisation in telecommunication services began around 1992, with the deregulation of telecom sector. The sole reason was to provide relief to telecom operators from the steep fixed license fee regime, the government gave an option to switch to the revenue sharing fee model. The Government allowed participation of private sector for all telecom services. It was far more challenging for India from being a government-owned monopoly to an industry with active private sector participation. As per the new licences, the operators were obligated to share a percentage of their AGR with the government as licence fee. The concept of AGR was finalised in 2001 and the telecom companies were liable to pay around 3-5 per cent of AGR as spectrum usage charges and 8 per cent of the AGR and licence fees.

The legal battle

It is ironical how the very policy that was brought to play has become a bane for the sector. The legal battle was regarding the definition of AGR – which is used by the Department of Telecommunications (DoT) to calculate the charges payable by the telecom operator. The operators were arguing that AGR should comprise revenue solely from telecom services, but DoT insisted that AGR should include all revenue earned by an operator, including that from non-core telecom operations like rent, profit on the sale of fixed assets, dividend, interest income and so on.

The 14-year battle finally came to an end with Supreme Court ruling in the favour of DoT thereby demanding a whooping amount of Rs. 92,000 crores. The hassle over defining AGR was dragged so long that the actual dispute amount now remains a minor proportion (25 per cent) of the entire dues that the DoT has been asking for. The Rs 92,641 crore includes Rs 23,189 crore as the disputed amount, Rs 41,650 crore of the levy of interest, Rs 10,923 crore as penalty, and Rs 16,878 crore as interest on penalty. Say three years ago, the total dues were just Rs 29,474 crore.

Just when the operators were reeling from a bruising tariff war, there came the AGR blow.

Business Players

Just ten years ago, India’s telecom was crowded with a plethora of players jockeying for dominance. There was a time when new entrants found it difficult to enter the market and make even a miniscule change and gain the market share. Tariffs were almost the same because all the major players formed a coalition where they decided what will be the optimum number of tariffs so that all the telecom giants are able to gain with it. Back in the days, 1 GB data was too dear to us, recharging it was quite expensive that all of us use the data so prudently because the cost of recharging was so high.

The Boom

Reliance Jio came with a whole ecosystem of services to supply – speed of internet data, powerful broadband networks and smart devices that were distributed at Rs. 1500, refundable after 36 months on return of the phone at any Jio store. This offer sounded a death kneel to the prevailing 2G and 3G phones available at that point. Reliance Jio was the sole telecom operator that offered fully data centric services, entirely supported voice long-term evolution (VoLTE) technology, which enables voice to hold over an online protocol (IP) network at a better speed than earlier 2G and 3G traditional networks.

Indian customers are very price sensitive. Price may be a key think about developing and emerging markets like telecom sector market in India. Reliance Jio has brought a revolution in Indian telecom sector by introducing free 4G data and voice calling and hence was ready to entice 100 million subscribers within one year of incorporation.

As Reliance Jio made the telecom sector bleed within the bargain it had been filling its pockets by brand image, customer satisfaction, value added services. The impact of Reliance Jio on telecom industry is so severe that it’s going to be termed as a revolution in Telecom Industry in India

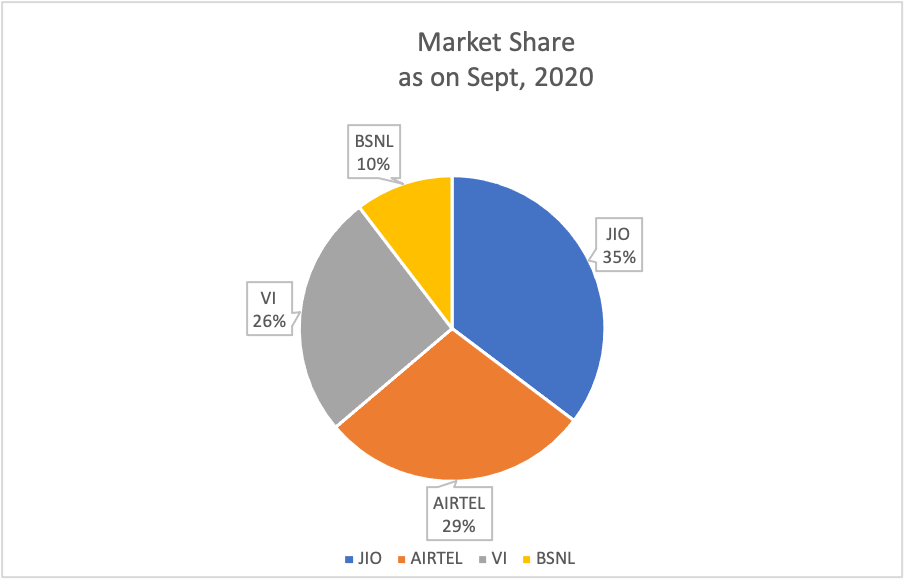

After a series of disruptions, mergers and variety of telecom players exiting the market, India now has 3 major players within the telecom sector – Vodafone Idea (VI), Bharti Airtel, and Reliance Jio. These three Telecom operators own 89.6% of the entire subscriber market share as of Sept 2020.

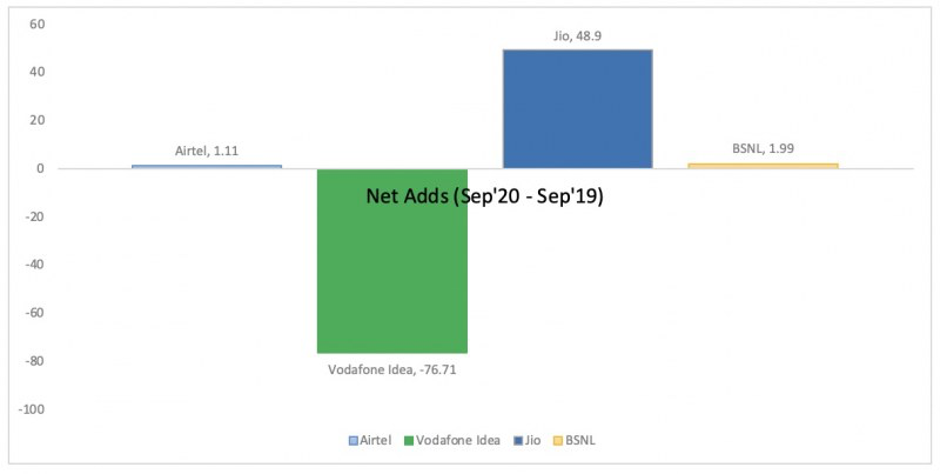

In the last 1 year, Jio has gained 48.9 million subscribers whereas Vodafone Idea has lost 76.71 million subscribers. Airtel has gained on the brink of 1.11 million subscribers whereas BSNL has gained on the brink of 2 million subscribers.

It looks odd but BSNL is growing despite the extraordinary competition from rivals.

The Survival

The apex court has allowed the operators to pay 10% of total past dues upfront and remaining 90% are often paid within the next 10 years starting 2022. The estimated liability for VIL could be Rs 5,000 crore by FY22 then an annual payment of Rs 7,000-8,000 crore for subsequent decade. Analysts at ICICI Direct acknowledged that while all the telecom players got to raise tariffs to pay AGR dues, VIL has already been suffering from cash burns and should find it difficult to satisfy the demand of annuity payment of Rs 8,391 crore from FY22 end onwards.

With Vodafone’s recent branding exercise, the struggling operator looks composed to battle. However, the question remains will it manage to regain its share? Although the rebranding assures on-lookers but survival during this deadly rock where the corporate has lost on the brink of 76.71 million subscribers is hard-hitting.

Particulars | Bharti Airtel | Vodafone Idea |

Deferred Spectrum Liabilities | 43,349 | 88,530 |

Other Debt | 73,963 | 27,320 |

Total Debt | 1,17,312 | 1,15,850 |

Pending AGR Dues | 25,976 | 44,680 |

Total Debt including AGR | 1,43,288 | 1,60,530 |

Debt Owed to the Govt. | 69,325 | 1,33,210 |

% of Total Debt | 48.4% | 83% |

Source – Capital Minds; All amount in INR Crs.

Vodafone Idea (Vi) owes quite 80% of its debt to the govt of India in sort of deferred spectrum liabilities. Generally, operators pay half the spectrum cost upfront, post which there’s two-year moratorium period. The remaining 50% is to be paid in equal instalments over subsequent 16 years.

Is hope still left?

A benevolent regulatory environment could help Vi survive and not create a duopoly. Already a partial victory on the AGR issue has provided some respite i.e., 10 years to ante up the dues.

TRAI is considering whether to impose a floor price for tariff – a bottom-line where the operators cannot introduce price below that, which technically TRAI should have done when Reliance Jio entered the market. this might help Vi with some relief from the bitter price competition initiated by Reliance Jio.

The average revenue per user (ARPU) has almost become pennies to what it had been before Reliance Jio, while operating expenses have increased thanks to the high-speed network – 4G. But to show its fortunes around, the corporate has got to increase its ARPU. This may require the corporate to plug strategically especially within the data business. A number of this realization on the part of the management is already visible within the company’s strategy.

If the corporate is fruitful in increasing the revenue, it comes hand in hand for expenses to rise. Vi will get to invest more in towers to offer an improved network. it’s during this framework that the approaching 5G spectrum auction assumes significance. Maybe a turnaround for Vi?

Even a rudimentary 5G network will cost a minimum of Rs 1.25 lakh crore for the equipment and Rs 50,000 crore for the spectrum. Thereby increasing the operating expenses and further by increasing capital-related annual expenses (depreciation) by Rs 12,500 crore per annum — Rs 10,000 crore on the equipment and Rs 2,500 crore for the spectrum.

Add to this the value of capital within the sort of 10% interest — Rs 17,500 crore per annum, the added expense on 5G jumps to Rs 30,000 crore per annum. Assuming that there are some running costs, which will be reduced further, this may still require the corporate to hit a revenue run-rate of a minimum of Rs 1 lakh crore per annum to interrupt even, quite 2x of its current revenue of Rs 46,000 crore.

In other words, this may entail a mean Vodafone Idea user to extend his monthly consumption from Rs 130 per month at the present to Rs 275 per month. But will he?

Without making the 5G investment, there are only two options left for Vi – either to chop costs aggressively and face the brunt of the competitors or to merge itself with the opposite two big players.

The key question is who will invest in Vi for the 5G network? Who will take the danger to take a position during a loss-making company? Here, Vi can follow the instance of Reliance Jio who didn’t purchase Reliance Communications but preferred a sharing model with Rcom – both for sharing the physical infrastructure like towers and therefore the spectrum. This saved Reliance Jio from being exposed to Rcom’s financial blows. Vi can adopt an identical structure, the investor will only need to invest for the initial payment for the 5G spectrum and obtain the marketing, branding done under Vi.

Follow Us @

{kind=link}