Now let’s take a look at some of the business numbers of CRED. In their first year of operations Nov’18 – Mar’19, CRED had a negative cashflow of around INR 118 Cr, and an operating loss of around INR 60 Cr. Most of their costs were in customer acquisition and retention cashbacks. Their cash outflow for FY 20 stood at INR 164 Cr. However, they also witnessed a INR 3 cr interest on deposits, signifying a large cash reserve which can fund their growth prospects. That is not all. Shah has been one of the few founders who has been able to raise capital during Covid-19 pandemic as well. They have raised around US$ 180 million as of April’20.

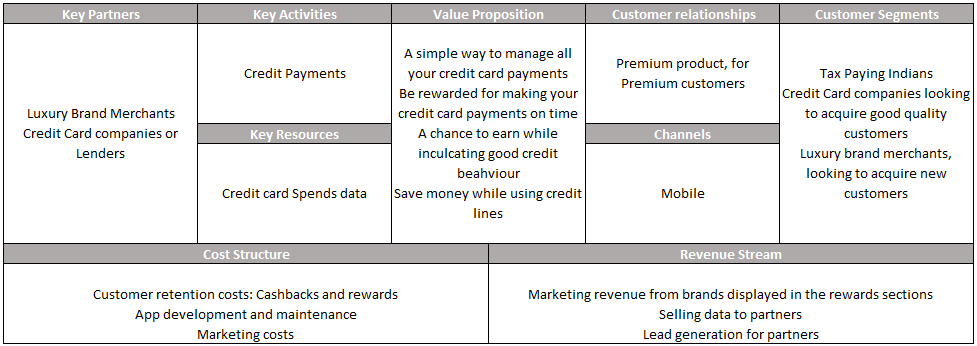

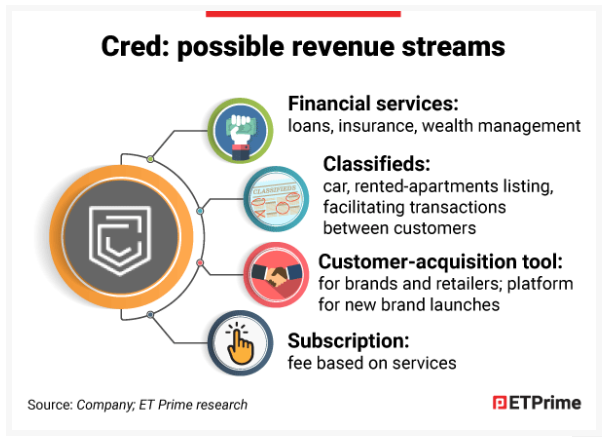

But, with so much of money flowing in, does CRED have a credible revenue source it can tap into? One of the means of revenue is through the promotion of allied brands. Brands Like Cult paid a hefty sum to be featured on top of CRED’s reward page, thereby driving a lot of traffic to their workshops. In fact, the success of these brands drew many more luxury brands to CRED’s platform.

Another model that CRED is working on is extending the credit line for monthly payments such as rent. So far, rental payments have never been done on credit. But with CredCRED’s Ren-to-pay, you can pay your landlord your monthly rent on credit for a flat fee to CredCRED. However, there has been no mention of the amount of fee income the company has received with this new feature.

CRED is also experimenting with extending credit lines to its customers for personal use. For the pilot, CRED tied up with IDFC first. The entire journey, from acquisition to disbursal was entirely paperless, a 100% digital, very quick and required no collateral. CRED and IDFC First did the underwriting based on the past payment and credit limit utilization patterns. Loans were capped at INR 5 Lakh rupees. The biggest selling point was that these loans were much cheaper compared to your typical credit card interest rates.

Another revenue stream CRED is exploring is to act as a sourcing channel for credit card companies and lenders. And because the customers on CRED are a bit on the premium side, with good credit behaviour they can charge up to almost 3 times the acquisition fees from your typical competitors like Paisabazaar or BankBazaar. Another reason for the premium is that the leads passed on from PaisaBazaar or BankBazaar are that of a credit hungry customer. Whereas the base on CRED, are customers who can take on extra credit but aren’t desperate for a loan! Which makes a world of a quality difference in the credit space.

{kind=link}