Market Cap: Rs. 1273 Crores Current Market Price: Rs. 1362

Company Overview

Lumax Industries is engaged in the production of stylish, high automotive lighting solutions. With strong collaborations and innovation, the Company accounts for a significant market share in the automobile lighting segment.

It has 9 state-of-the-art manufacturing facilities all across India. The company has 2 R&D centres in India and 1 Design centre at Taiwan. The growth has been catalyzed by more than three decades old collaboration with technical and financial collaboration with Stanley Electric Company Ltd, Japan, a world leader in Vehicle Lighting and illumination solutions. The company’s business operations span across four-wheeler, two-wheeler and farm equipment segments for leading OEMs. At the end of Q1FY19, the company had a net worth of INR 381 crores. Today, 5000-strong work force of Lumax have taken automotive lighting to an exemplary level in the Indian automotive industry. The company offers a range of Automobile Lighting Systems and Solutions for Four Wheeler, Two Wheeler, Trucks, Buses, Earth-movers, Tractors and a variety of diverse applications. As a leading company in the automotive industry with the latest technology and expertise to manufacture world class products, it aims to make most out of the opportunities in the near future. Through Lumax Charitable Foundation, the company engages in Corporate Social Responsibility initiatives for improving access towards Education and Healthcare of the disadvantaged communities around it’s plants.

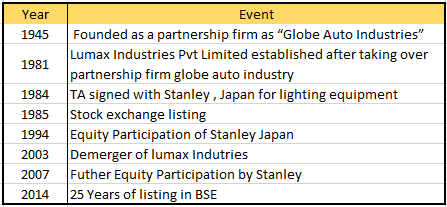

Lumax Industries History

Manufacturing Units & Research Centre:

Total 28 Center including 9 Manufacturing centers, 3 R&D facility and 1 Overseas Design Facility.

Industry Overview

According to a report published by McKinsey in September 2018, the Indian automotive industry aspires to triple in size by 2026. Optimism pervades all vehicle categories – passenger vehicles, commercial vehicles, two-wheelers, and tractors. This exciting forecast for automotive manufacturers also implies healthy growth for auto component manufacturers. The auto component industry now aims to quadruple in size by 2026 from USD 51.2 bn in FY18 and grow six-fold in terms of exports which stood at USD 13.5bn in FY18.

Market Shift

Automobile Industry has shifted towards implementing BS – VI norms, these norms will make automobile energy efficient and reduce the pollution arriving out of it.

Considering this in Automobile lighting sector the share of LED lighting will increase as more and more OEMs will be compelled to use LED technology lighting, also LED lighting gives good looks to the automobile.

Market Share

Lumax Industries is supplying to almost 90% of OE customers in India

i. Passenger vehicles 4 W: Market Leader, 55% Market share

ii. Passenger vehicles 2W: Market leader, 37% Market share

iii. Commercial Vehicle: 80% LED Lighting market share

iv. Revenue – 35% LED and 65 % Conventional Lighting

Competitive Advantage

i. Established player and market leader in the automotive lighting industry

ii. Tie up with Stanley , Japan in providing the technology for manufacturing of LED

iii. Developed 3 fully operative R&D center

iv. Manufacturing units established near major automobile factories

v. Back to back tie ups with most of the vendors

Revenue Drivers

i. LED Lighting trend growth amongst the automobile buyers

ii. Growth in industry, Industry estimated to be quadruple in size by 2026

iii. India will be 4th largest automobile manufacturer in coming years

Margin Drivers

i. Currently 61% of LED components are imported, plan to develop indigenous lighting system in coming years this will improve margins.

ii. Developing newer and in-house innovative technology through R&D centers which will cut down the cost of manufacturing.

Financials

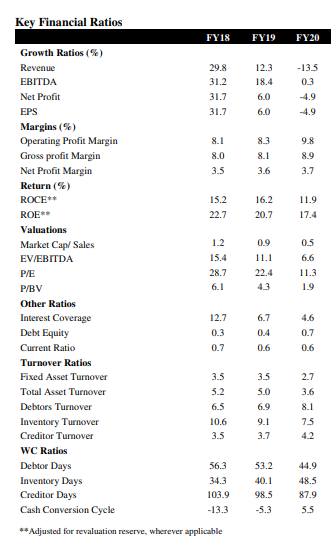

The revenue growth in FY 18 and FY 19 was robust however due to auto market slowdown in FY 20 revenue has been declined but the growth trend in auto sales nos has again peaked up lately as a result growth in topline will be seen in coming years.

Even though the revenue has dipped the OPM is increasing steadily from 8.1% in FY 18 to 9.8 % in FY 20. ROCE and ROE nos are good and seems to be peaking up again in FY21.

Valuations ratio has cooled off in last 3 years suggesting that it is fairly priced now.

Company is expanding and is building more capacity as a result debt seems to be slightly increasing, this will go down as auto sector revives.

Figs from CD Equisearch report

Risk & Challenges

i. Technology: Lack of appropriate technology competence Mitigation – R&D facility and JV with Stanley for having access to worlds most advanced technology

ii. Competition Risk: Mitigation – Long term relationship between leading automobile manufacturers, the ability to modify auto-component designs along with undertaking initiative to reduce cost enables it to be leading player in the segment

Valuation & View

It is estimated that the growth in revenue will be around 15% for a couple of years with the margin rising and reaching double-digit because of the R&D, reducing imports and cost-cutting measures. Revenues will also increase due to the rising ratio of LED lighting in product mix In FY 19 ratio is 35: 65 which will be improved to 65:35 in FY21 for LED and Normal Lighting respectively.

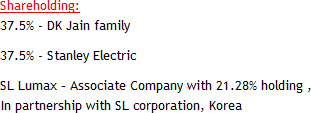

The company is operating since the last 86 years in this segment and its market leader, managed by strong management and industry expert. Promoters are well versed with industry and market leader at the global level (Stanley, Japan). Company is having a robust balance sheet and has proven capabilities. Promoter stake has increased in the last couple of years in the company to 75%. The share price is down 45% from the top due to the slow automobile sector growth, but the cycle will change, and the company can be a multi-bagger.

{kind=link}