Compuage is a wholesale distributor of IT related products and services. I will delve deeper and start with the industry and company analysis that will inculcate almost all aspects of the business.

Industry Analysis

As the reader would have understood that the company’s business will be impacted by two industries i.e. Information Technology and Wholesale Distribution. I will be talking about these two industries in detail.

1. Information Technology

Majorly, the Indian Information Technological (IT) industry works on the outsourcing model. The industry is driven by companies which are predominately service organization in contrast with the ‘product’ companies you find in the west particularly, the Silicon Valley.

Inherently, the biggest asset for these companies is their workforce which India is at a superior advantage due to one of the highest no. of educated engineering graduates in the world coming out of universities every year, which are well equipped in English and can be trained and employed at the lowest cost.

With a 55% global market share of ~ $200-250 billion global services sourcing business, India is the leading player in the world, giving credibility to its advantages as mentioned above. India also accounts for 75% of the global digital talent in the world.

Indian IT and BPM sector’s revenue is ~ $ 191 Billion estimated and is growing ~ 7% y-o-y, estimated to reach $ 350 Billion by 2025. The domestic IT industry’s revenue is close to $ 44 Billion and export revenue ~ $ 147 Billion in FY20.

The latest developments in the IT sector has been evolving in cloud computing, big data, analytics, AI and IoT. It is estimated that India’s cloud market will touch $ 7.1 Billion by 2022, a three-fold jump from 2020. This is truly the most growing area in the IT industry. The Saas (Software as a service) sub-industry also is estimated to grow by 36% annually, reaching $ 3.3-3.4 Billion by 2022.

What makes India the No.1 destination for global IT outsourcing?

- Huge population size with growing middle class (estimated to be reach 475 million by 2030), young population (with an average age of ~ 28-29 years) and rising disposable income, rising penetration of mobile phone users (estimated to be 36% in 2022 from 26% in 2018) and rising internet penetration with the cheapest data being offered by telecommunication companies.

- The operational delivery of the Indian IT and BPM industry encompassing all channels- onshore, offshore and nearshore. Rising startups and ~ 16,000 firms operating in India, gives a huge scope in in-service delivery and project inflows.

- As already talked about broadly, India currently has over 6 million graduates and the industry has the reputation of being the largest private sector employer, close to 3.7 million projected recruits.

- India being a digital hub- both in terms of execution and offering new enhanced service delivery. This has been clearly seen in the pandemic when the industry was quite resilient (visible in the financial results) with catching on to trends in cloud infrastructure and businesses moving to WFH models.

Opportunities

Technology is dynamic and is ever-changing with the increasing pace of innovation. The business dynamics are also changing with the change in vendor delivery models, moving from opex to capex model, as capex requirements limiting in size due to the proliferation of cloud infrastructure.

The large players are being more dominant as they are gradually converting themselves from service providers to full-fledged digital and platform solution providers, positioning their services as products.

- The pandemic is shifting consumer preferences away from offline to online delivery models and people are spending more time interacting online via their tech-led hardware devices.

- Cloud Computing: The pandemic has accelerated the pace of these trends. One such trend is cloud computing which not only has become a necessity for companies working on WFH models but also drastically help them in growth of their bottom line and reduce capex requirements/ reducing the costs associated.

- Mobile Penetration and other hardware: As already spoken, the smartphone penetration in the country has been growing at an above rate and this pandemic has increasing the rate of adoption. Estimated to be about 829 million smartphone users in India by 2022

My take and COVID effect

The growing trend of the IT companies in India moving to the emerging technologies is the step forward. We will see companies adopting increasing digital solutions, converting their businesses online and focusing on digital offerings.

Indian consumers, (as already observed from numerous data points) will shift in an increasing pace of doing things online and the data points according to my estimates are under-valued. The unorganized as well as MSME Industry will get a big push towards digital, due to the expectation of partnership between Jio and WhatsApp.

The COVID pandemic has been a boon for the IT companies and ascending the growth, particularly cloud related services. Cyber security is one more area which is increasingly benefiting from the WFH concept because business operations moving towards different ‘areas’ and hence increasing scope of malware attacks.

2. Wholesale Distribution

Wholesale distributors basically are the intermediaries who buy ‘goods’ in whole sale quantity from the manufacturers/vendors and sell them to retailers and resellers. This can be done on cash or credit basis, working capital and inventory management being the most important parts of the business.

Trends

- Competitors in the industry are coming in, most prominently the Direct 2 Consumer firms and online web portals like Amazon, Alibaba (prospects look bleak), Walmart-Flipkart, IndiaMart etc. Moreover, brick and mortar retailers also find it ‘cheaper’ to cut through the intermediary and directly source the products from the manufacturers.

- With the availability and usage of data analytics and big data, manufacturers can themselves understand customer trends, which they used to depend on the distributors.

- The growing need for efficient warehouse management, indirectly inventory turnover management and reducing wastage due to the business being on thin margins.

- Digital offerings: The industry is into B2B space, which calls for efficient management of the operations, focusing on being lean. This drastically calls for increasing adoption of digital, which will give retailers an omnichannel experience, better product offerings and information, online tracking and inventory management.

- Distributors have to distinguish themselves by offering more value-added services like giving manufacturers more insightful customers data/trends and sales training to retailers.

- Rise of automation in handling retailer’s data and emerging retailers that can be prospective customers. Automation helps in better product delivery, order management, staffing and inventory management

One of the major areas that are important to look at in the industry is its logistic cost, for mainly tangible products delivery as well as how close the warehouses of the companies operating in this industry are to the retailers.

Going into the narrow business of IT distribution industry in India, historically there has been two companies which have dominated, namely Ingram Micro India and Reddington India (not listed in India).

However, in recent years due to favorable factors (mentioned above), lot of companies have come into the national front with partnerships with different brands.

Brief Note on IT Products (guidance from Atul Mehta- CMD, Compuage)

The present industry size is Rs.70,000 crores + contributed by 10 major players. The IT hardware and mobility including enterprises are converging into brands like Apple which is both into IT and mobility. The IT consumer sector doesn’t seem to be growing but enterprises seem to be growing as well as mobility. The enterprises which include cloud is into investment stage, industries are embracing but there is a slow momentum, in the way of adoption. But there remains a huge runup.

Businessman’s Hat

We look at stocks by wearing a businessman’s hat and will look at this business in the same way.

The wholesale distribution industry, according to our firm belief, is or will be in decline as the competition in the retail industry consolidates. Retail giants will expectantly do backward integration and/or directly talk to the manufacturers, cutting away the distributor in the middle.

Moreover, there is a big push of going digital, which will hamper tradition distribution channels and will call for cost optimization as well as re-thinking on the part of the management regarding logistical cost. Also, the introduction of robots and drones in factories as well as warehouses, will reduce employee cost and move towards more efficient operations.

The key for retail (ultimate customers), like before, is the management of working capital which we think will become in a better position due to reduced demand, with a simple reason of moving digital and being less dependent on physical stores.

Compuage Infocom

Now, we will be discussing about the business in detail, and deciphering all the important tenets of the company, including qualitative as well as quantitative aspects.

History

The company in 1987, started its humble beginnings as a corporate reseller, of computer consumables.

In 1992, the company expanded its offerings to include peripherals and became an authorized dealer.

The company then in 1995, started importing IT hardware and established regional offices in Delhi, Kolkata and Bangalore.

In 2001, the company expanded into distribution and got listed.

In 2006, the company expanded aggressively with some campaigns and showcased its product offerings to ~ 600 resellers across India.

In 2012, the company also forayed into international business, establishing its presence in Singapore to serve the SAARC region.

In 2018, the company also established its presence in Sri Lankan market, office in Colombo.

In 2019;

Business

Compuage in simple words is a technological distributor, with business broadly divided into two parts: technology distribution and hardware support services.

Technological Distribution

The company sells IT hardware and software products to resellers. It bridges the gap between vendors and resellers by providing an additional service of vetting the resellers for the vendors, whose ‘brand reputation’ depends on how the product is actually delivered to the final consumer (customer experience).

Hardware Support Services

The company also provides after-sale services, with extended product offerings like warranty services, logistics, technical assistance and field engineering support.

Products and Services

The company is a technological distributor, with 11000+ VARs and presence in 600 cities.

The company to differentiate itself from competitors, by providing training and business solutions to resellers and system integrators- including training, supply chain expertise, technical, financing and enterprise solutions. ~ this is an important differentiator for the company, leveraging relationships with its resellers.

Corporate Governance

As we have mentioned in our past reports, corporate governance is one of the key tenets while looking at a business. Corporate Governance tells the investor that there is a high possibility that the business will be run by taking into consideration the interests of all the stakeholders.

Mr Atul Mehta is the Chairman and Managing Director (CMD) of the company. He completed an undergraduate degree in Commerce from University of Mumbai and his Masters from University of Portland, USA.

Mr Atul Mehta seems like a leader who is in total favour of adaptability. He accepts the fact that the sale of computers has been falling and also called for resellers to start focusing on smartphones and enterprise businesses. He also accepts the fact that the traditional mindsets have been changing and change is the only constant. He also calls for people to adopt new technology. He has been in this business since 1987.

He also accepts the premise, that the company would have shuttered if they wouldn’t have embraced changes in the 90s. ~ This shows that the leader at the top is a visionary, but also one has to look at the actual execution, which we will delve deeper when we will be analyzing the numbers. He is 57 years old.

Bhavesh Mehta is the COO of the company and is the younger brother of Mr Atul Mehta. He is 45 years old and I believe, is being groomed to lead the company after the latter stops working. He has over 20 years of experience in the industry. He has done his undergraduate and a graduate degree in Commerce, specializing in Marketing.

Corporate Governance

Generally, it is good to have the promoter shareholding >50% (in this case ~ 58%) in the company, which basically reaffirms the belief that promoters and retail investors interest will be aligned.

There are no shares that are pledged by any of the Key Management Personnel. This is important, because in case there is any financial trouble to any of the KMPs, like some personal financial obligations, the lender can either sell the pledged shares in the market, which put pressure on the share price or retain the shares, which threaten the stability of the management of the company as the control shifts.

Compensation Information

The KMPs positions mentioned above as well as some other executive directors, are based on contracts and salaries are fixed for 3 years after which the salaries are changed. There is also a mechanism of targets that have to be met by KMPs which will entitle them to other benefits- monetary.

Overall, corporate governance seems fine. Only, provision being the promoters of the company, mentioned above don’t have a specific background in technology or supply management ~ not a big concern as they both have 20+ experience in the industry, but nevertheless just wanted to point it out in open.

One positive has been seen that the company in FY20 recognized COVID pandemic and the salaries of the promoters have been cut by ~21% and no % change in the salaries of employees. This had been done to reduce the employee cost of the company which forms 1% of the company’s direct cost.

Disclosure Style

The company hasn’t disclosed how its various business divisions have been performing over the years. Yes, the revenue part has been bifurcated into different components, but how EBITDA and EBIT and Net Income contributions have been? ~ hasn’t been disclosed.

Some Important Points to consider

The company indirectly focuses on end consumer i.e. like me and you and through its enterprise business, focuses on corporations. So one needs to understand that if there is a systematic risk ~ of course, both the parts of the business will be affected, but also one needs to take care about the industrial growth as well as how GDP and economic scenario outlook looks like. There is a direct correlation between the economic scenario and the performance of the enterprise business which is a growing and the focus area looked on by the company.

One of the things I came to know that the company is conservative in its approach and recognizes the importance of working capital in its business. If there is a receivable from a party which is due, the company doesn’t do business with them until all the dues are cleared. This really brings efficiency and introduces discipline into the operations. This may impact the relationship with the parties in the short term but the quality of the business and working capital requirements should remain better.

The company’s cash flow situation also majorly depends on the interest rates prevailing in the country. This is due to the credit given to the channel partners, which depend on interest rates in the economy. Due to the low-interest rates, it is possible that there will be a delay in the cash flows going forward, simply because the channel partners can postpone the commitments due to low obligations.

The company also conducts marketing activities for its principles which are partially funded by them.

In this industry, the company in one of its conference calls admits, that size matters a lot. They have to either raise debt or equity to grow even 10%. If they are okay to grow by 5-8% (which they are not), then they have to raise capital. This is negative for the investors going forward because to grow the company, the equity will be diluted or debt situation will deteriorate. Now, due to wafer-thin gross margins, the company also doesn’t enjoy operating leverage, so even if the company might increase sales by double-digit late teens, still it won’t be able to earn much of the bottom line.

If one looks deep, the company has either increased share capital (equity- through a preferential allotment, bonus or new shares) or raising debt. The company also raises money through FDs – taking advantage of low-interest rates prevailing (took in FY20)

The company also a standardized way of managing the receivables and bad debts problem. They have two policies for vendors. One is stock rotation: if something is moving slow, then every quarter the vendors can return a % of that inventory back and fresh stock can be ordered or the 2nd policy of supporting through the price ~ can tweak the price. Here, one important thing to add: Compuage doesn’t take the inventory risk, the manufacturers are responsible if some product is not moving at the desired pace.

The company has suffered no bad debt till now (past 12 months) but also have taken a bad debt insurance policy (credit risk insurance) against which there hasn’t been any claim. (FY19) The bed debt no for the past 5 years (in terms of policy payout 3-4 crores but depends on the revenue. The worldwide credit insurance policy covers only 85% of receivables ~ THE BIGGEST RISK FOR THE COMPANY.

The Q4 numbers as observed by me has always been higher (last 5 years). I was thinking of the possibility of channel stuffing. Through my research, I came to understand that in Q4 vendors get added up and hence revenue goes up.

The company in the overall IT distribution industry has 10-15% (6-7%) market share (can’t be ascertained due to unlisted players and due to different product mis/offerings and a lot of unorganized players) and has grown by 18.5% CAGR over the past 10 years since 2019, well above the industry average of 5-8% CAGR.

The company is not doing well in the mobility part of the business, with a revenue contribution of 13-14% whereas for the competitors it is ~ 25-30%. Provided, in the IT products overall, mobility has been growing the fastest.

2 Cents on the industry structure: Difficult for any business to come in for 4 reasons: 1. Infrastructural demand, 2. Brands willing to sign up to new distribution channels- you have to be the best company to fill the gap 3. Distribution channel knowledge and product knowledge 4. Relationships and network.

The company regularly pays a dividend, total outgo comes out to be Rs. 2.5-3 crores… Now, this cash could be used for debt repayments, as that will be more judicious use of money (due to the high cost of debt). The focus of the company has been on growth, hence according to us, it doesn’t make much sense to distribute cash to shareholders. ~ Capital Allocation concern.

Also, when asked, Mr Atul Mehta didn’t agree for the buybacks because he wants to focus on growth. This is a negative, as the effect of buybacks and dividend will be effectively the same. In Q4FY20, when COVID impact was there, still the company declared Rs. 1.3 crore dividend (10%). This can also point towards the angle of giving monetary compensation to the promoters due to the decrease in a fixed component. An educated guess, but this is really problematic.

The company also is not of the view of growing through acquisitions but by acquiring or partnering with brands. ~ This seems positive because acquisitions are always a dangerous deployment of capital.

The company also saw a downgrade in its ratings due to increasing debt and not ‘at time’ capital infusion problem, which later it received in the form of debt.

The company also realizes that the future is cloud solutions and believes that it still in a very nascent stage (August 2019), going foreword it will be beneficial for the company due to the subscription-annuity model of cloud solution rather than traditional server infrastructure requirement.

Customer distribution

No client caters to >10% of the company’s revenue, top 5 <15-16% of the revenue. This reduces the concentration risk and also the bargaining power of the customers.

The company works on broad-based models and understand the importance of diversification, it caters to 12,500+ resellers, retailers etc.

The company also recognizes and understand the vitality of the Indian markets and hence points out that they plan to focus more on Category C and D areas, which have grown at a higher rate than the metro counterparts. (also this can be due to the infection rate spike seen in metros)

What Disruption?

The company strongly believes that any online player won’t be able to throw away offline players like Compuage, because of their ‘go-to-market strategy’ and low-cost distribution.

They provide all type of services to resellers as well as retailers (mentioned earlier). They are proud that they are surviving at ~ 3-4% margins and hence no competitor can disrupt them. Sure, they accept that they have to evolve and embrace the changes but they firmly believe that they have a strong moat, and won’t be out of business.

Case in point: Samsung, although having 80-90 warehouses and having countrywide distribution went with them due to their go-to-market strategy and thin margins ~ which do give us some hint about their moat.

The differentiator in Cloud Business

The company in its pursuit of being different has launched a platform wherein resellers can opt for the cloud product they want to subscribe to. The company has also tied up with Microsoft to distribute its cloud offerings – which is a big positive for the company. This shows that the company is trying to deliver on its statement about the importance of the cloud business. The company operates at ~ 8% margin in cloud business – which the company believes is its potential ‘star’ performer.

They also try to differentiate in other businesses by offering more support to resellers in terms of technical – pre-sales team and other support. Also, the company aims to be a one-stop solution for the IT needs of resellers.

No Exclusivity

The industry players work on multiple-distribution channels and the company as well the industry doesn’t have any exclusive partnerships with any of its brands.

Priorities of Management

One of the most important priorities of top management is to focus on core operations. The management (like in this case) might be holding a big chunk of the company but it is not the responsibility of the promoters to comment about stock prices.

In one of the conference calls, Mr Atul Mehta was asked about the fair value of the company. He not only not commented but straight away refused and told the analyst that it is not his job but the market people to decide that.

Major Risk Unwinding

One of the biggest risk/challenges faced by the company is the industry’s dependence on China for IT-related products so there will be some supply-side disruption in the short to medium term. But the company is sure that there is no option with the industry as well as the economy as most of the production is done in China and the company also believes that there won’t be any price impact nor any import duties levied.

Also, the company’s revenue exposure of Chinese brands, working out of China is measly 2-3%, but the company in its latest Investor conference call of Q1FY21 reiterated that the company won’t be affected much as it depends on manufacturers where they can manufacture its products. The segment, prone to these problems is the hardware ~ which forms the bulk of the revenue for the company and we strongly believe that the company is underestimating this.

Numbers and More

Under this section, we will be taking the readers on the number-crunching side as well as some other distinct facets of the business.

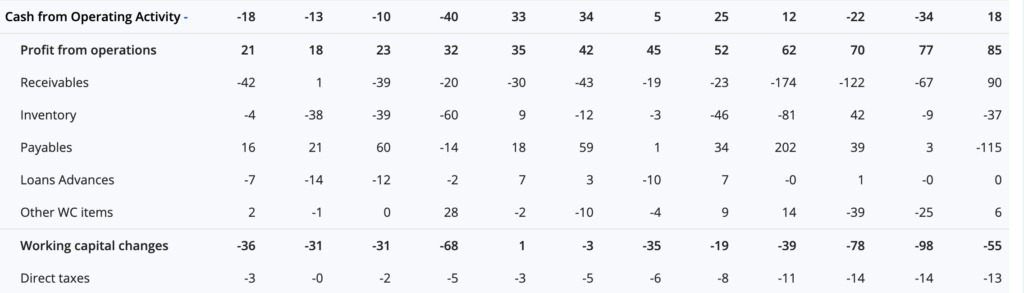

1. Working Capital Cycle

The working capital cycle in basic lingo means how much time the company takes to convert inventory and receivables into cash. There is no exact figure wherein one can define an ideal working capital cycle, but generally, the cycle should decrease over the years, indicating faster cash conversion.

It is computed by adding no. of inventory days and no of receivable days and then subtracted from payable days.

The working capital days in FY20 stands at 53 days, a trend observed over the years ~ seems positive, due to working capital cycle decreasing, due to tight control over the inventory days as well as receivables management.

In the latest quarter, the days increased due to two reasons: the resellers have been affected due to lockdowns- nation-wide and local (hence the strategy of moving towards Category C and D areas, which has been seen not having many infections) and also the NBFCs and banks reluctant to lend working capital loans. 2nd reason due to product mix change.

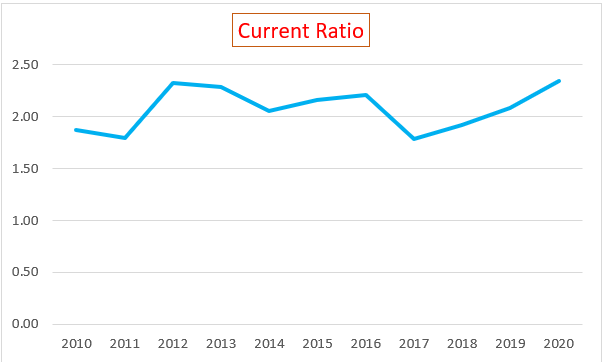

2. Current Ratio

The current ratio is important to gauge, which will give us a glimpse of how is the short-term position of the company, concerning liquidity.

The company, it seems like, has managed its liquidity profile quite well. I have taken a conservative approach and taken out some of the components of the asset side and include some of the components in the liabilities side. Effectively, the company’s assets have always been ~ 2x than the current liabilities.

Now, there is one contention here. The receivables forms bulk of the current assets (45-50%) which if turned bad can hurt the liquidity profile, but the company has taken credit insurance against them which effectively covers 85% of the value, so even if we assume 30% loss in terms of bad debts, the impact will be there but still the ratio, after my calculations, will be >1.

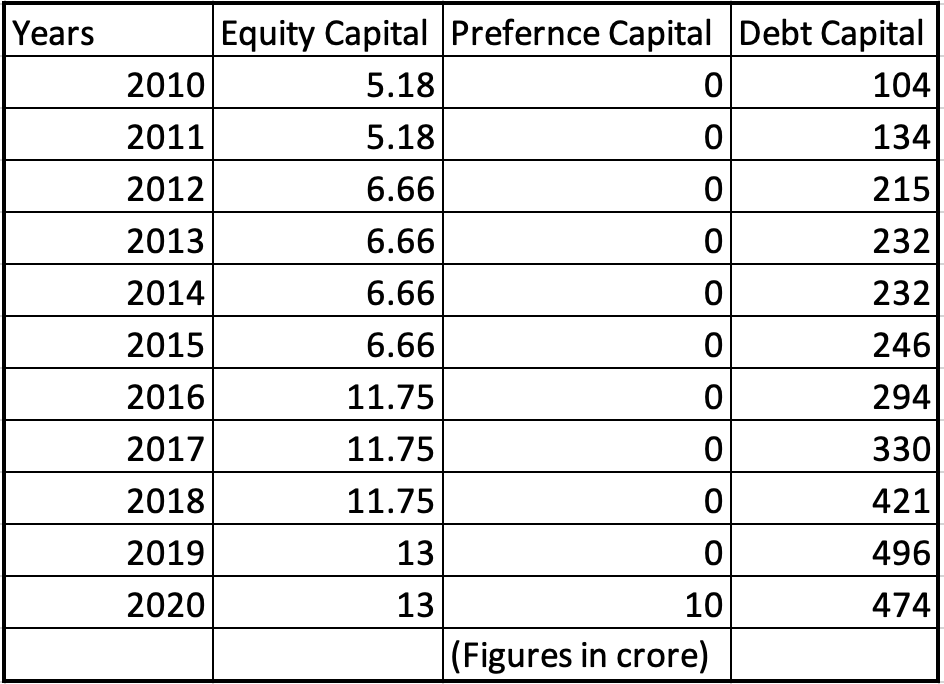

3. Capital Structure

One of the most important trends to look over the years is the capital structure which effectively means how the company is getting funded over the years. This is very important to look at especially in this company because it is in its growth stage and the CMD of the company has stated in every conference call, the need to raise funds if they have to grow at a higher rate than the industry.

They don’t look at reducing debt in the future and are looking at raising more debt, and not doing equity dilution further.

This is concerning. The company has consistently raised capital either in the form of equity (in 2-4-year gaps) or debt (every year). Recently, the company’s debt rating has also been downgraded to A- with a negative outlook simply because of its deteriorating capital structure.

The cost of debt is the lowest cost of capital, but one has to be careful with regards to how much debt one can sustain. With EBITDA margins of 3-4%, it really troubles us and going forward really makes us anxious, about the company’s sustainability.

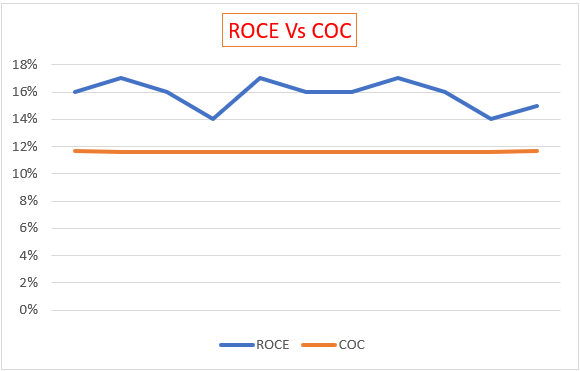

4. ROCE Vs Cost of Capital

The return on capital means the return one can expect on the total capital employed in a particular business, and cost of capital, as the name explains, the cost of total capital employed by the business.

The cost of capital came out to be ~ 12% and on average the return on capital employed comes out to be 15-16% over 10 years. There is very little money that the shareholders are virtually earning. Though due to the company entering into cloud business and hardware services being a bottom-line generating business has the potential to grow the ROCE at the time the same time the company will be looking towards raising more debt capital in the future, which they are also of the view that the cost for them will also rise, from the current north of 11% (due to rating downgrade)

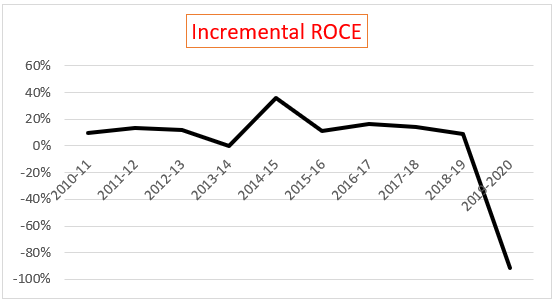

5. Incremental Capital growth vs Incremental Capital Return

This comparison is quite important to do as the company has consistently raised capital and one should see how much return this capital has given.

Before analyzing, I will request the reader to ignore 2013-14 and 2019-20. This is because in 2013-14 no incremental capital was raised and hence the return was generated and in 2019-20, the debt was repaid which made the figure negative even though there was a positive return figure of Rs.88 crore. On average (with some deductions) the incremental return has been in the range of 15-18% which throws a positive light on the capital raising spree of the company but again, the cost of capital remains elevated, which dampens the return by a few percentage points.

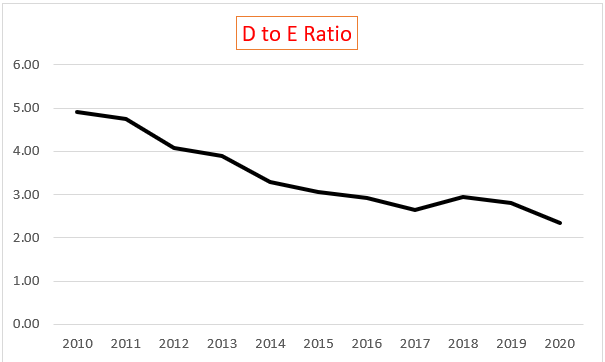

6. Debt to Equity Ratio

The debt to equity ratio has been decreasing due to accumulation of reserves, but still the ratio >2, which seems dangerous, and the company has given the guidance of increasing the debt capital in their capital mix, further in the future.

The risk can be mitigated because of the company’s focus on physical safety and security division and cloud solution division which are higher-margin businesses and can deliver accelerating incremental net income.

This should be strictly monitored going forward, with a time frame of 3-5 years.

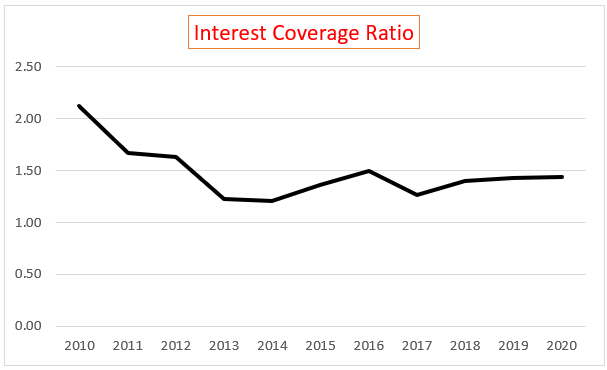

7. Interest Coverage Ratio

Due to rising debt infusion and the rising cost of debt capital, it is important to see whether the return generated by the company will be able to fulfil its debt obligations.

A big worrying sign, the company’s interest coverage ratio has been declining is in the latest year, is just ~ 1.5x.

This was expected, but we think that this will deteriorate further down the line due to increasing capital requirements and rising portion of debt capital, the financing which have to be serviced.

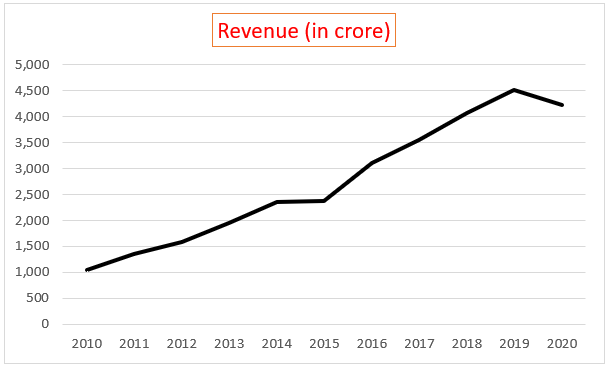

8. Revenue Growth

The company’s revenue is divided into 5 verticals- IT consumer contributes about 34%, IT enterprise contributes about 46%, cloud contributes about 1.5% and services have a very small topline. It contributes less than 0.5%. It is more of a bottom-line driven business.

Service business- negligible top line, bottom line-driven- this is according to the Q4FY20 investor conference call.

The company has managed to increase its revenue by 14.89% CAGR over 10 years, if we remove FY20 due to the total March sale of 0 which impacted the year, it shows a ~ 18.5% CAGR growth.

The company’s focus has been on the cloud business, started this business ~ 18 month back but it didn’t disclose the segment-wise revenue for Q1 FY21, due to the Pandemic impact.

The cloud business still needs capex and other ongoing expenses. This should be monitored closely as it has ~ EBITDA Margins of 8% (highest). The company also is trying to focus on Physical safety and security like CCTVs etc which forms a part of the IT enterprise part of the business.

One of the areas where the company might not be as enthusiastic as the hardware services business. A bottom-line margin of 20-30%, it contributes 0.5% of total revenue with 69 stores already opened. This should be looked upon by the company, in a more aggressive way ~ we think this also seems like a capital allocation problem.

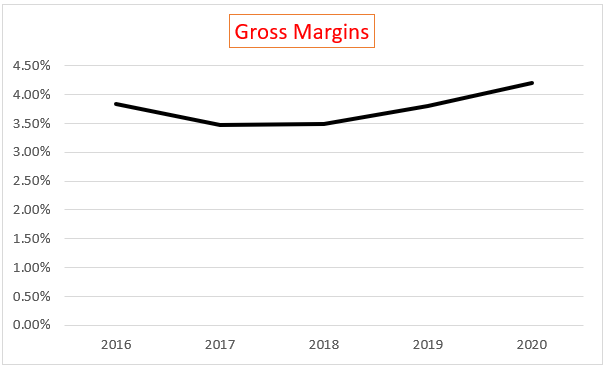

9. Gross Margins

This is quite positive to see, the gross margins have been consistently rising and according to Mr Atul Mehta, this is quite sustainable going forward.

In the coming years, the company will focus on reducing the employee cost as well as other expenses wherever cost rationalization will be pursued.

| Years | Gross Margin |

|---|---|

|

2016 |

3.83% |

|

2017 |

3.47% |

|

2018 |

3.50% |

|

2019 |

2019 |

|

2020 |

4.21% |

The purchase of hardware and software IT goods form the bulk of COGS (~95%) of the cost which is quite difficult to reduce, but the company is also negotiating with the vendors due to cost rationalization efforts ongoing.

10. CFO Vs Net Profit

The company has consistently generated profits over the 11 years starting from 2009 to 2020, but the company has not able to convert them into cash. This is major because of heavy working capital requirements of the business as well cost of financing being paid.

This is one of the major reasons, that the long-term shareholders (most revered group) haven’t earned much over these 10 years. They have earned on the dividend front but as pointed out earlier the company has not been making prudent capital allocations as that amount can be used for other better reasons.

| Stock Price CAGR | |

|---|---|

|

10 Years |

-1.94% |

|

5 Years |

-3.67% |

|

3 Years |

-18.80% |

|

1 Year |

52.53% |

This is also hinting towards a deeper point, that indirectly, the company is also not having ‘return’ opportunities for that cash that they are giving out to shareholders over the years.

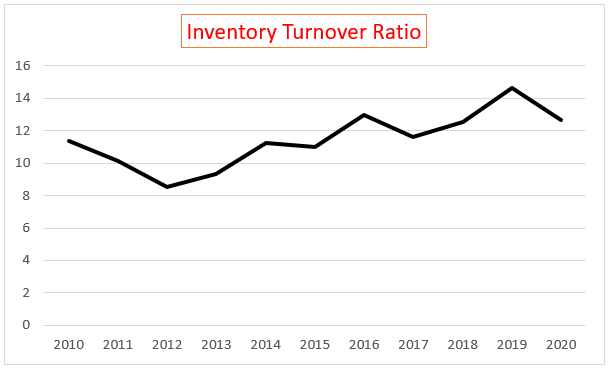

11. Inventory & Receivables Turnover Ratio

This is an important number to look at a company where inventory forms the bulk of the cost of goods sold.

Inventory Turnover Ratio should increase which in simple words mean that in a given year how many times the inventory has been ‘churned’- effectively how much time that goods on the shelf have moved, in other words, higher the ITR higher the sales.

A positive trend should be a rising ratio, effectively implying better inventory management.

The company has seen some down years, wherein the inventory turnover fell but over 10 years the inventory turnover has increased.

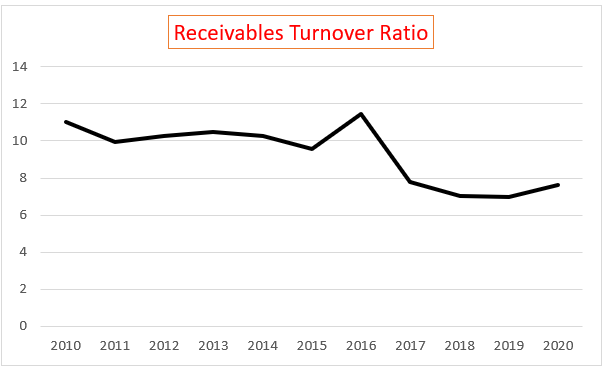

Now, this should be seen in conjunction with the receivables turnover ratio, there is a possibility that due to rising inventory turnover, the receivables turnover also rises, which means that the company selling goods fast but most of the sales are turning into receivables but not cash.

The ratio has declined over the years. This is negative for the company as the company has been able to increase the sales with somewhat declining quality of the incremental sales. The company has not been able to convert its credit sales into cash.

Receivables Turnover ratio indicates how many times in a year the company has been able to turn the receivables into cash

Now, this is congruent to our earlier conclusion, that the company has also not been able to generate free cash flows – implying not a good inventory and receivables management.

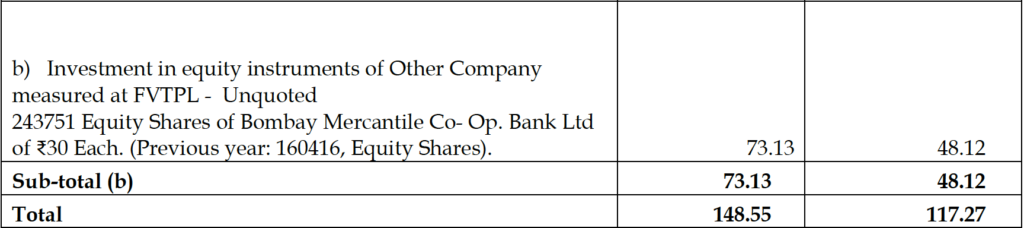

Questionable Investment

The company has invested in the Bombay Mercantile Co-Op. Bank Ltd. Upon being asked by an analyst, the company answered that the relationship is long term, and as the bank extends credit, the company has to subscribe to the equity share capital of the bank. The amount is insignificant.

The matter was not disclosed completely by the company but we presume as the company takes on more debt, it had to subscribe to more capital – again which might not be a good use of its capital. Also, it is an unrelated business as well as an unquoted investment which also carries illiquidity; hence the company won’t be able to sell it quickly without discount.

This should be monitored on a q-o-q basis due to the capital raising plan by the company in the form of debt.

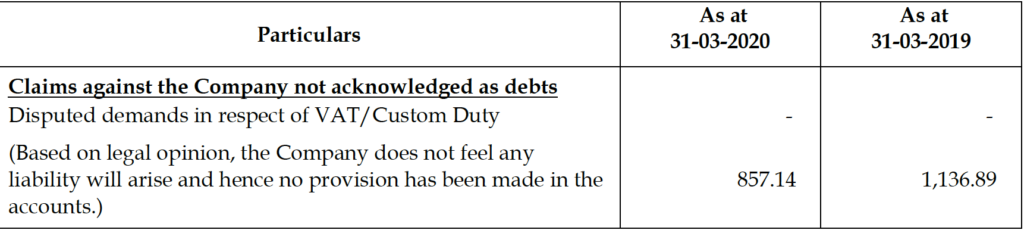

Contingent Liabilities

The company consistently had contingent liabilities over the years. This latest figure (mentioned above) forms ~ 2% of the core revenue of the company.

The company hasn’t provided this figure in its books.

We believe that this will not impact the company a lot due to the insignificant amount relative to the company’s core revenue.

Valuation

We are firm believers that the markets are supreme and are reasonably valued most of the times. But we are also of the opinion that if stocks are looked upon as ‘partnerships of a business’ then taking the businessman’s hat, one could earn good amounts of return on the capital invested over the years.

Now, the business interests should only be purchased if there is growth potential and it is reasonably valued. The latter part will be looked upon under this section.

We will try to value this business by some model, which will include certain conservative assumptions. We induct conservatism, due to the market risks present as well as according to the idiosyncratic risks present in a particular business.

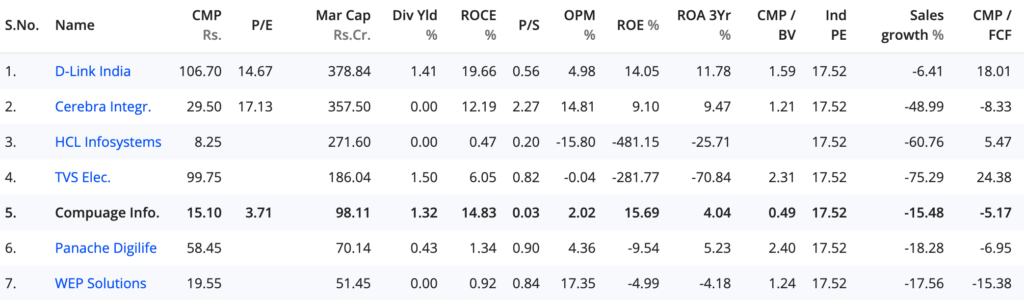

Competitor Valuation

On a comparative basis, the company seems ‘cheap’ or in other word undervalued.

The company after certain adjustments (from the figure mentioned) has a PE ratio of ~3, as compared to the industry average of 17.52. This according to us, is due to the company being a late entrant in the industry, where size matters a lot. Thus, the market is not valuing it as much as the bigger counterparts and discounting its small size- hence not re-rating the multiple.

The market cap is also one of the lowest in the industry.

On a positive side, the company has earned one of the better ROCE figures, now this can also be understood in the context of COC, as researched, the bigger counterparts’ COC is much lower than Compuage.

Interestingly, and somewhat in the obvious, the company’s ROE is the best due to low equity dilution in the recent years and more of debt capital, which directly provides the interest expense benefit as well as leverage.

The company Price to Free Cash Flow ratio is negative, simply because the company is on capex cycle, as the company aspires (delivering as well) to grow its revenue (business) on a higher rate than the industry.

The company, according to us should be valued on a Price to Sales basis due to greater emphasis on sales and minuscule profits and FCF and CFO.

The company’s present P to S ratio is ~ 0.03, assuming sale growth (long term average) of 19% CAGR ~ to be conservative we took the FY21-22 growth in revenue to be 15%.

Assuming the P to S ratio gets re-rated by 5%, due to the growing nature of the company as well as entering into attractive areas, the market cap that we are looking at ~ Rs.150 crores which come out to be ~ Rs.23 per share. We can take a margin of +/- 10%.

This sounds a big jump from the present ~ Rs. 100 crore market cap but the way the company has given guidance and the nature of business the company is in, it makes a good sense to the company being valued at the market cap that we expect.

Of course, there are risks present, which have been detailed in this report which might harm the re-rating of the stock.

Conclusion

One must be cautious of the risks present in the business and also should closely monitor the things that have been mentioned in different places. One should also not be bogged down by the exact numbers and should like a businessman who is looking at a 100 crore investable business.

Disclaimer:

The information and opinions present in this report are for educational purposes and not to be construed as any form of an investment recommendation. The author, as well as publishing website, is in no way responsible for any form of loss to anyone who takes any form of decision based on this report

The information/data present in this report is best to the knowledge of the author and any misrepresentation should be considered unintentional.

Follow Us @

{kind=link}