Cimmco Ltd, a listed Indian small cap company is into wagon manufacturing, trucks and other industrial goods. In this report, I will be talking about two segments – wagon and trucks. This is because the company mainly deals in wagons. The company has forayed into truck manufacturing as well, by entering into a strategic partnership with Titagarh Agrico Private Limited. (TAPL).

The company (i.e. Cimmco Ltd) has also got an industrial license by the GoI for manufacturing of defence products in FY16.

Wagon Industry

The Indian wagon industry’s main customer is Indian Railways, a GoI entity. The railways has been predominately been in the government’s domain. This has impacted the industry due to irregular demand, decremental orders and possibility of predatory pricing by the competitors in the industry. The industry is characterised by the bulk orders, but as already stated irregular orders by Indian Railways, which make the financials of the companies quite volatile.

Indian Railways usually call for bids for the tender order for wagons. Earlier, IRs used to allocate the tender quantity to L1-L6 bidders (L1 being lowest to L6 being the highest, ascending order) on a fixed ratio basis. The rest balance of 40% used to be allocated on the basis of execution track record and capacities. Now, as per revised scheme, IR will allocate the tender to L2 at the same price as L1, provided the capacity of L1 is fulfilled.

This policy change will impact the industry as a whole. This is net credit negative for the companies. According to an Indian Ratings & Research report, this will consolidate the industry and also increase the working capital requirements of the industry.

The IR also used to supply some free items which used to account for 40-50% of the raw material cost of the wagon manufacturers. This was stopped after FY18-19 due to supply constraints.

The IR have also come up with some raw material specifications which call for sourcing from RDSO, Rail Wheel Factory, etc.

The current government, also on 1st July 2020, announced to start with the privatisation of railways in India, starting with 151 trains in 109 pairs of routes. The private train operators are required to start operations from April 2023. They are allowed to procure locomotives and trains from any source. This seems like a positive sign for domestic wagon manufacturers due to increase order visibility. (and for the wagon manufacturers as well)

Trucks Manufacturing

Trucks manufacturing started in India back in 1961. Before that, the demand was fulfilled by imports. The turning point for the industry was post Green Revolution 1960s when the local production accentuated.

The agriculture sector is main industry where the demand for tractors come from. Good monsoons, increase in MSPs for various crops and non-farm activities like manufacturing and construction also boost the demand for trucks in the country.

In the farming sector, due to increase in mechanization, trucks play a vital role in cultivation. The industry is capital intensive in nature, used as transport for displaying labour and also used for electricity generation.

In 2020, when the entire market demand is at abysmal level and automobile industry is still recovering, the trucks demand have gone up due to normal monsoons and increase demand for farm related products.

Business Highlights

Cimmco Ltd has been predominately been in wagon manufacturing business. The nature of the business has already been discussed in the industry analysis.

Let’s talk about some characteristics which will help us understand the qualitative nature of the business better.

The company doesn’t seem to be enjoying economies of scale, due to small size. Due to the recent merger announcement with its parent i.e. Titagarh Wagons Limited, it is expected that due to shared cost economies (i.e. two firms sharing a common cost basis), the company can take advantage of scale.

The companies in the industry can only fight on price, there is no visible differentiation. Therefore, the base and the business should be big enough to manufacture on large scale so that the company can bid at lowest prices and play on sufficient volume. In the years that I studied, the company has mainly lost out to competitors due to predatory pricing.

The company is also majorly dependent on one customer, Indian Railways, which dramatically increases the barging power of the customer. Other customers are the private players, which is expected to increase due to the encouraging announcements by GoI.

Moreover, due to the recent policy change by GoI about the wheel procurement that has to be done by Rail Wheel Factory, Umesh Chowdhary in his latest investor conference has told the audience that it is a big pain because most of the times the factory is not able to deluver and hence they have to rely on Chinese imports, which has started getting delayed due to the recent India-China border standoff.

One point that we want the reader to know is that, the company has a defined benefit plan for its employees, that is unfunded i.e. it is in the range of 6-10% of the market cap of the company or ~ 2% of total fixed assets. We believe that this can be easily funded by the company.

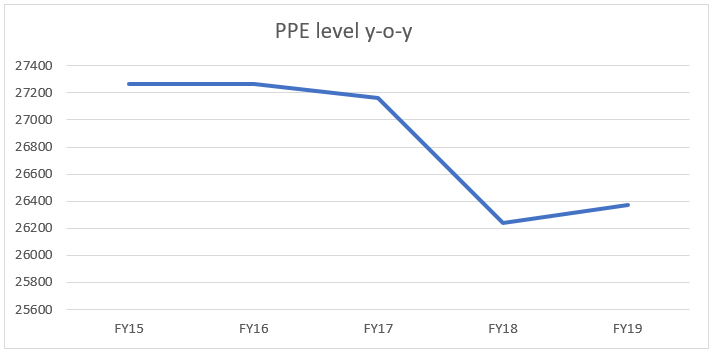

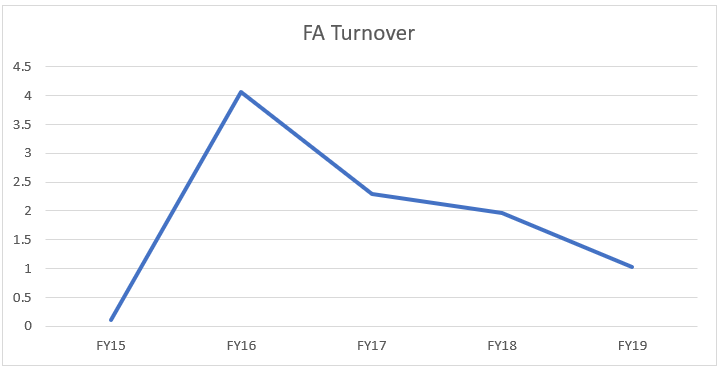

To understand a capital intensive business, we will generally look at PPE (the fixed tangible asset part of the business). Relatively over the years, the PPE level has declined. I have not been able to decipher why the PPE is going down but when we churn more, we see a more disturbing trend.

The company’s ability of using its fixed assets efficiently has been declining. It show a sharp jump from FY15 to FY16 and then has been on declining trend.

This can be attributed due to the company entering into strategic ties with TAPL for trucks wherein they will be issuing their land to TAPL and the latter will be providing the company with 3% of the sale price. This decreases the need for building more capacity for truck manufacturing. Though, if we see the PPE graph, post FY18, the trend seems to start going up. This is due to the amalgamation process completed and TAPL and Titagarh Capital Private Limited (TCPL) merged with the company.

Moreover, the company has also some leasing business wherein it leases wagons from subsidiaries of the parent company (TCPL), to IR. This arrangement also calls for less usage of fixed capex.

These business characteristics doesn’t affirm any substantial observation. Sure, it gives a hint of declining capex requirement and company gradually shifting its business to a relatively asset light business.

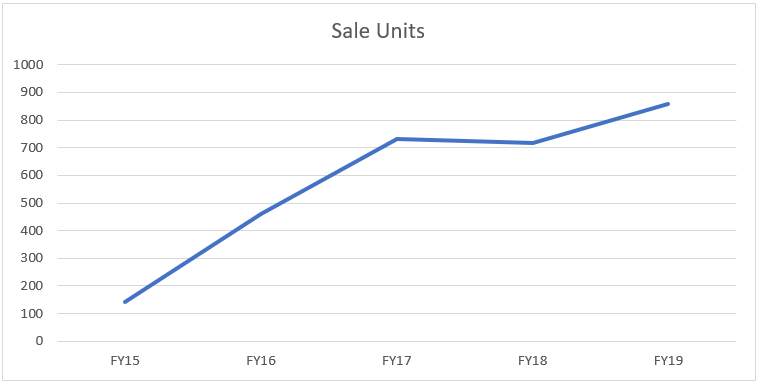

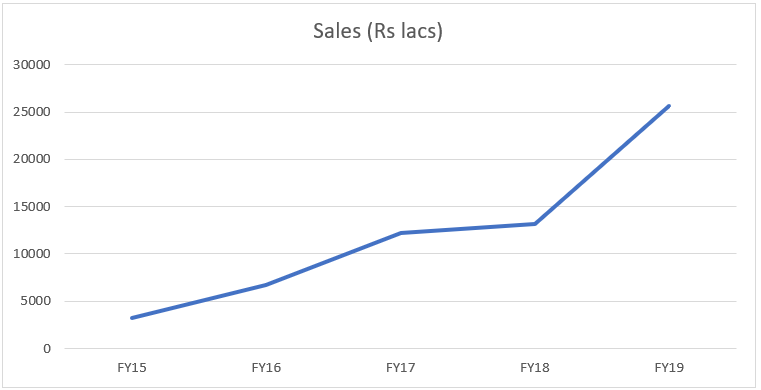

Let’s look at sale figures and value and see how the top line is getting affected.

The revenue (net of excise duty) has been on the rise both in volume and amount figures. If the reader goes deeper in the numbers, there was a decline of units from FY17 to FY18. However, the sale amount increased (not a big increase, but increase nonetheless). This was due to per piece realisation rose in the past 4-5 years.

The company is also gradually moving its customer base and trying to diversify to more private customers. The sharp increase from FY18 to FY19 which can be seen is surprising at a time when the orders declined from IR by ~ 27%. This is attributed to two factors, the favourable order procurements by IR which increased the order book by 260% and favourable bulk orders from private players (numbers not mentioned)

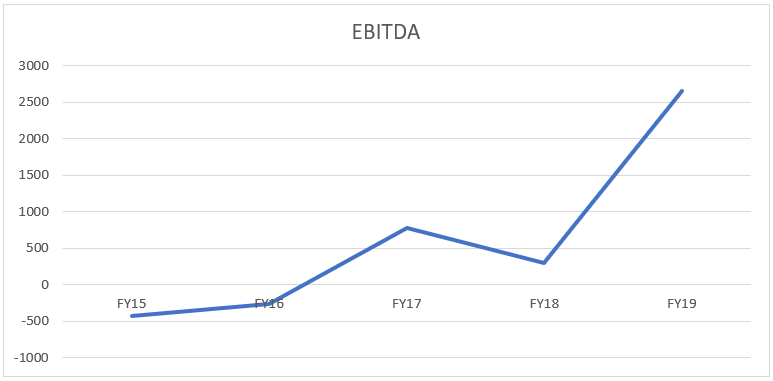

The EBITDA figures have been adjusted to give a fair picture of the company. We won’t talk about EBIT because we want to exclude the depreciation and the debt part. (being capital intensive business/industry).

The EBITDA figures are on the rise which gives us a hint of the company turning around. Moreover, with the merger with the the parent, the company will add to its existing capacity of 2400 unit, ~ 6000 units capacity.

While reading the annual reports, we observed a big over hang on the company:

Contingent Liabilities

Looking at FY19 report, when we look at the contingent liabilities notes:

There are legal disputes in totality exceeding ~ Rs.1600 lacs which have not been provisioned for by the company. The company has a belief, that it is probable, not possible that the action will succeed.

The company had an export licensing agreement, wherein they imported certain components, subject to fulfilment of certain export obligations within a prescribed time frame. Now, due to closure of factory and cancellation of the export orders, the company was referred to Board of Industrial and Financial Reconstruction (BIFR). The company had paid Rs.85 lacs and the balance Rs. 11 lacs had been provisioned for in the previous years. The company is not able to determine the true liability due to various licenses sought earlier and hence no accurate provision on the books.

The company also has a claim against IR for the 887 wagons that it leased to the latter. The lessor of these wagons was originally TCPL, who made a claim against the company. IR didn’t pay for the lease and hence there is a back to back claim against IR, who have now asked for the possession of the wagons by paying 1% of the acquisition cost.

TCPL along with the company, in-front of the sole arbitrator, had asked for Rs.5000+ lacs for the delayed payments (including 22% p.a. interest). The company has not made any provision for this claim due to the back-to-back claim and the merger announced recently.

Some Important Ratios

We look at businesses that help us achieve decent returns on the capital employed.

- ROCE

We will be looking at the ROCE of the company over a time period to gauge how the company has performed using its capital base.

This calculation has been performed by doing some adjustments to reflect fair value, to the best of our assumptions and knowledge. ROCE has been historically negative which is big cause of worry. The company has not been able to generate returns on its capital base. But, we see the ROCE shot up in the recent years due to probable recovery in the company’s operations.

Debt Situation:

The company has some long term borrowing obligations as stated below:

i. The company, from the latest available annual report, has a long term borrowing to the tune of Rs. 9334 lacs carrying an interest of 9.2-9.85%. This has some loan covenants and is also secured by a first pari-pussu charge by way of mortgage on plant and machinery and all the fixed assets at the Bharatpur site, Rajasthan. The loan covenants were not fulfilled by the company on 31st March 2019, there were minor non-compliance and management is confident that it is a minor episode. This has to be repayable in b/w September 2018 and September 2023

ii. There was a term loan to the tune of Rs.1994 lacs which was repaid in full. This was also secured by a first pari-pussu charge on land owned by the company at Gwalior and also backed by a put option of TWL. In case of default, TWL had to pay the full o/s amount.

iii. There are also some related party loans which carry interest rate of 11% p.a. In FY19, the interest payment paid on borrowings of the company was Rs 333 lacs to the parents and Rs 270 & Rs 353 lacs to TCPL. ~ This seems like a troubling point for the company.

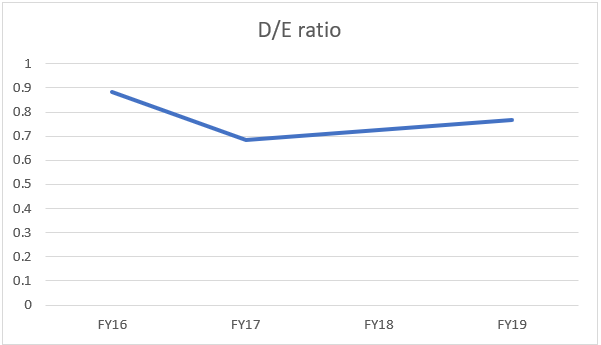

Looking at the debt to equity situation, the situation of the company looks positive but the trend over the years has been up reaching ~ 70% debt to equity.

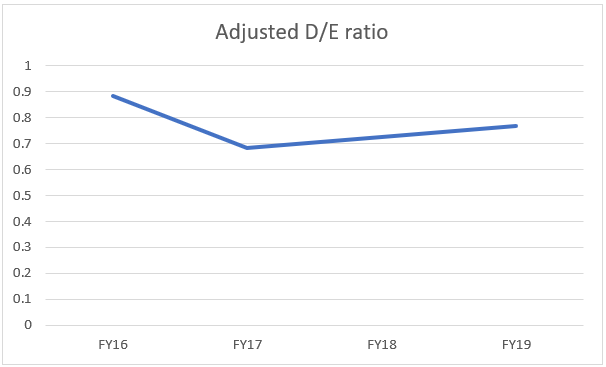

To give a more conservative and true picture of the company, we have adjusted the debt to include contingent liabilities, disclosed by the company.

The graph doesn’t do justice with the increased debt level vis-a-vis equity. The numbers in absolute amount has increased exceeding ~ 70% debt to equity. This is a threat to the company’s operation.

In one of the annual reports, the company declares that the parent will support the company’s operations due to the dismal performance in the recent years.

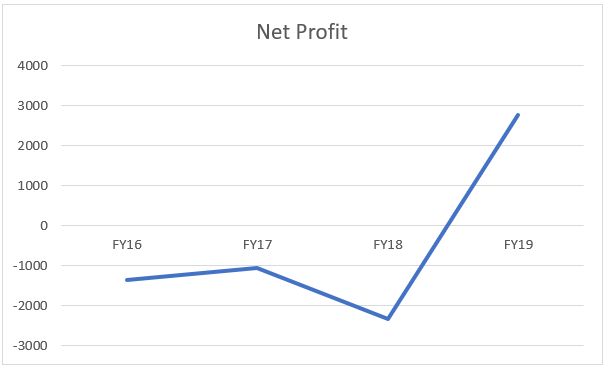

Looking at the net profit above, gives a bad picture to an investor. The company has been generating losses for the past 3 years. The latest year (that we have information of) has been good for the company. Net Profit has increase to ~ Rs.2800 lacs.

The drastic increase is due to the benefit of the past negative DTL, due to the tax benefit being generated by the company in the past years because of losses. (~ 2670 lacs)

Due to updated numbers not available officially from the company, we will also look at quarterly data to gauge some more information about the company.

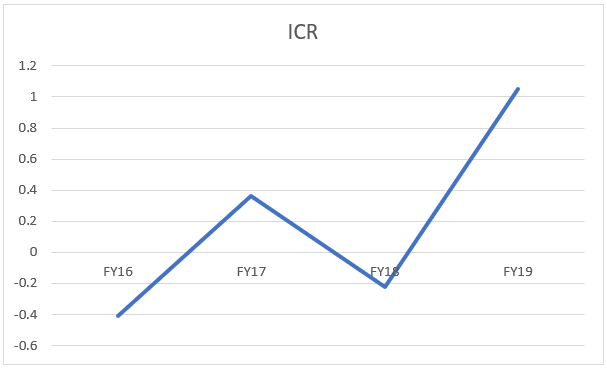

One important ratio, that we will be looking is Interest Coverage Ratio. This is simply because the company doesn’t have positive EBIT for some of the years. This is a red flag and a cause of concern for the company. To give the reader a picture, we have shown a graph of the ICR.

In the latest year (i.e. FY19), the ICR seems to be favourable for the company but still at a dangerous level. We have adjusted the ICR to include finance cost as a whole which include some lease operations and financial obligations that the company has to fulfil.

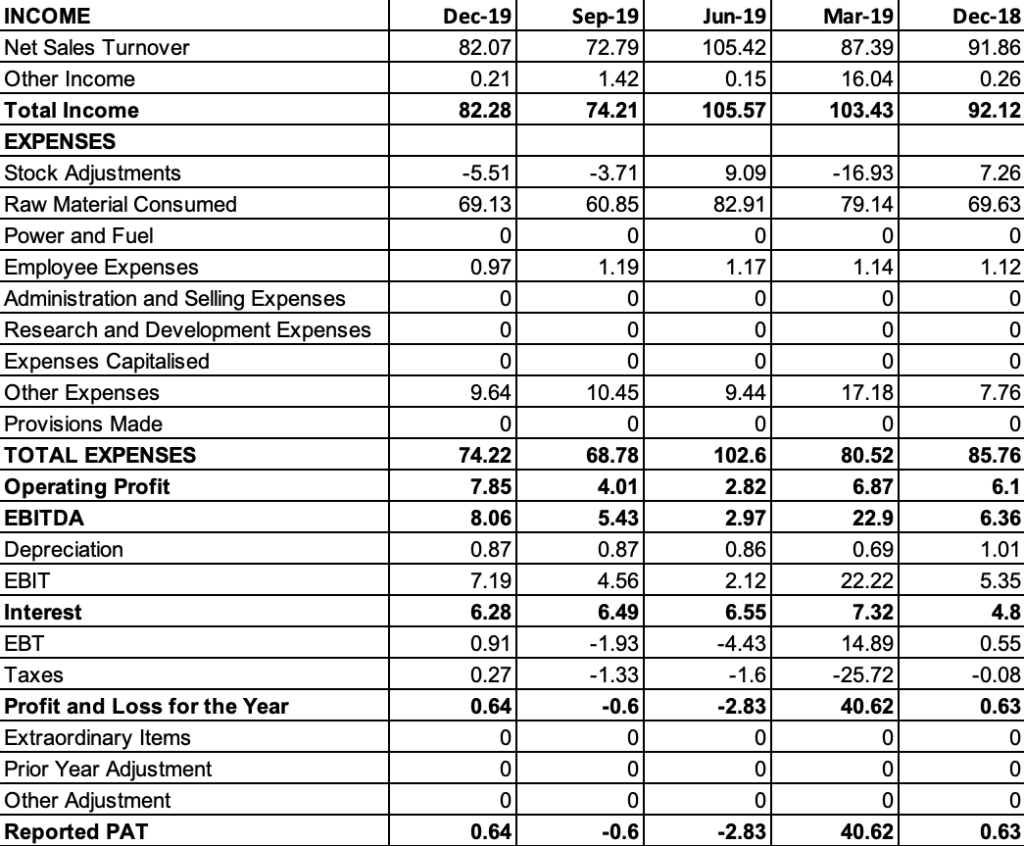

Below, is a summary of quarterly figures the company has reported.

The profitability seems to be going up, by looking at all the metrics- Net Profit, Operating Profit and Gross Profit. Revenue also increased by ~13%. The most favourable numbers that was recorded was by EBIT, increasing by 34.41% and EBITDA by 48.43%. Though, we generally don’t look too deeply in quarterly numbers, but it gives us a hint of a slight recovery in the business.

If we look at interests payments vis-à-vis EBIT, the situation is dangerous. Constantly, the ratio (EBIT to Interest payments) have been <1, which introduces huge default risk.

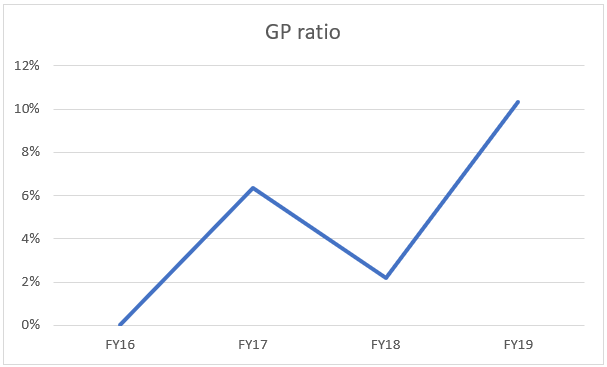

One huge risk the company faces is the raw material. If the reader looks at both the annual as well as quarterly numbers, one would see that the raw material cost (major part- steel or stainless steel) forms the chunk (70-80%) of the total direct expenses of the company which is a huge drain on the company’s gross profit ratio (though it is showing increasing trend)

The latest figure that we calculate is ~ 10% of revenue which is quite low.

The company will be sufficiently affected by steel prices and that introduces raw material risk for the company, steel industry being quite cyclical in nature. The steel prices are majorly affected by prices of oil, historical trends, shipping cost and its own demand-supply dynamics.

So one has to be quite careful and make educated guesses about the steel industry as a well while looking at the company.

Corporate Governance

The company is headed by JP Chowdhary, Promoter and Non-Executive Chairman; Umesh Chowdhary, Promoter and Vice Chairman and Anil Kumar Agarwal, CFO.

The salaries of the above are within the prescribed limits and too modest according to the industry average. The salaries of above range from Rs.5 lac to Rs.18 lac, including directors fees.

We will be talking about JP Chowdhary, who started Titagarh group in 1982. He is presently 79 years old. He has held chairmanship of Confederation of Indian Industry (CII). He started his career as an account at BHEL. In the Titagarh district of Kolkata, he visited Britannia Engineering Company, whose steel floundering unit was closed since the past 17 years.

IFCI was the main creditor of the BEC and Mr. Chowdhary decided to do something about it because he believed that with a proper roadmap the factory could be revived. He gave a presentation to IFCI and was able to convince them.

He was introduced to a lot of investors and also took a loan against his own equity as well as partnered with his neighbour and started the Titagarh Group in 1982. There were lot of problems involving local politics as well as sceptism on the part of investors who didn’t believe that a factory that had been closed for so long could be functional.

But it did happen and today the group has a turnover exceeding 3000 crores. “My journey through entrepreneurship has made me visualize things in their wider perspective and not get bogged down by petty issues and shirk from challenges,” he concluded while talking to Entrepreneur magazine in 2017.

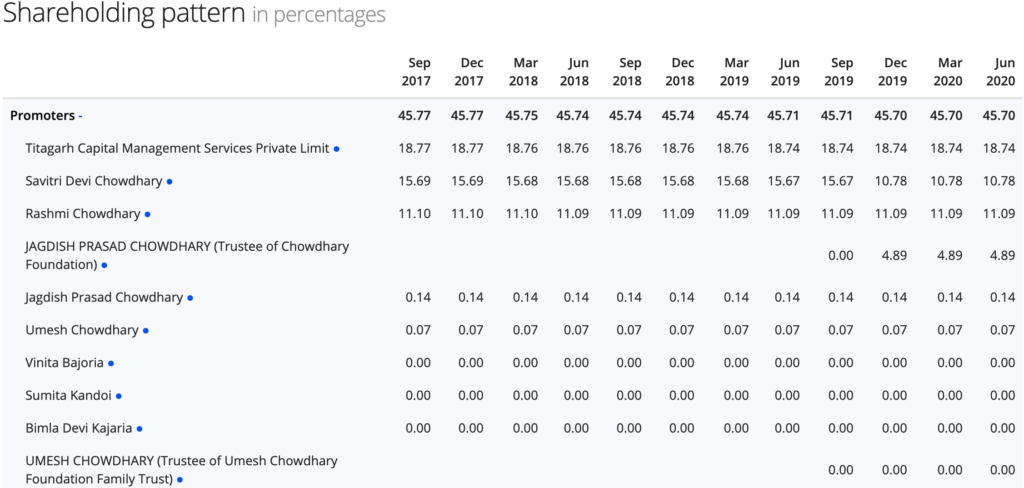

The shareholding patter of the company seems favourable with 75% of the shares are held by the promoters. There was a sale of around ~ 5% by the company’s parent, TWL because of the amalgamation process initiated by the group.

No shares are pledged of the company by any promoter.

We won’t be comparing profitability ratios with the managerial compensation as the salaries are fixed.

The chart below shows the shareholding % of the TWL. The promoter Chowdhary family owns a substantial % of the parent, which gives us confidence regarding the interests aligned of the KMPs with the small investors as well as other beneficiary stakeholders of the company, as a whole.

Audior’s Opinion over the years

The company received a qualified opinion in FY16, due to a claim that an amount of Rs. 3952 lacs will be received by the company, the case of which was pending in court. The auditor was unable to comment on the recoverability as well as impact of it on the financial statements of the company.

The company also received a qualified opinion in FY17, the company disclosed that it has a receivable from IR to the tune of Rs.854 lacs, against a credit loss of Rs.3097 lacs which was adjusted in opening retained earnings. This issue was pending in court, and auditors were unable to comment on the recoverability and consequent impact on the financial statements of the company.

In FY18, the auditors were changed because of fulfilment of 5 years (has to be changed due to the legal requirement), from S.R. BATLIBOI & CO. LLP to Price Waterhouse & Co. Chartered Accountants LLP.

The company received a qualified opinion in FY18, the auditors flagged material weakness in the internal financial controls of the company’s operations. This is due to the fact that some of the claims receivables provision did not operate effectively and hence, the auditor couldn’t ascertain whether adequate provision against claim receivable from a customer, have been made by the company.

A material weakness implies that there is a possibility of material misstatement of a company’s financial statements or reports might not have been detected or prevented on timely basis. ~ A huge red signal.

The company received an unqualified opinion from the auditors with regards to the internal financial controls as well in FY19.

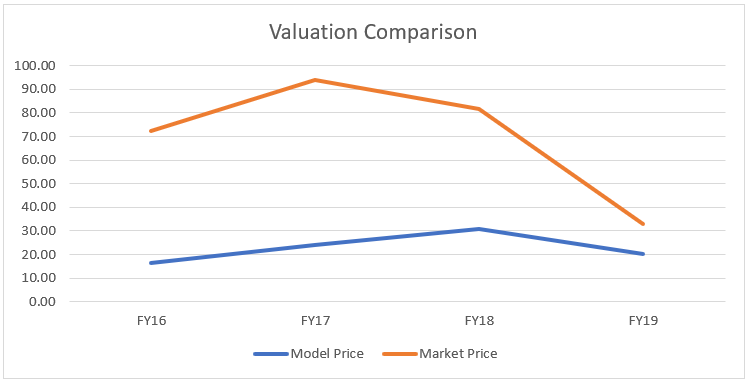

Valuation

The company doesn’t generate free cash flows. The company has been making losses. We will try to value the company by taking the assets approach as company is in a capital intensive business. We will doing some adjustments like including contingent liabilities and not including certain assets, which we believe will reflect the true picture of the company’s financial position.

This valuation takes the traditional book value approach because of obvious reasons. This is the most conservative approach used, adjusting for contingent liabilities and using tangible assets plus the cash on hand. All the liabilities have been included in the model which again calls for the conservatism used. The latest year data that is available i.e. for FY19, our model calculates the price to be Rs.20 with a range of Rs.10 to Rs.30. The present market price of the stock in the market is Rs 27.

Interesting Events

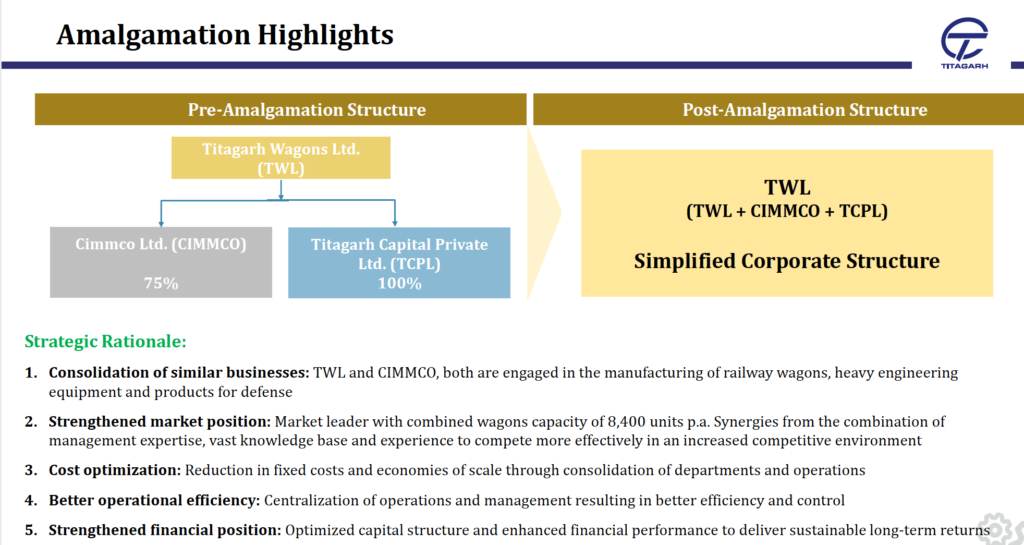

Before talking about the merger, the company had a manufacturing unit in Bharatpur, Rajasthan and the primary business was manufacturing and selling of wagons and heavy engineering products/ projects.

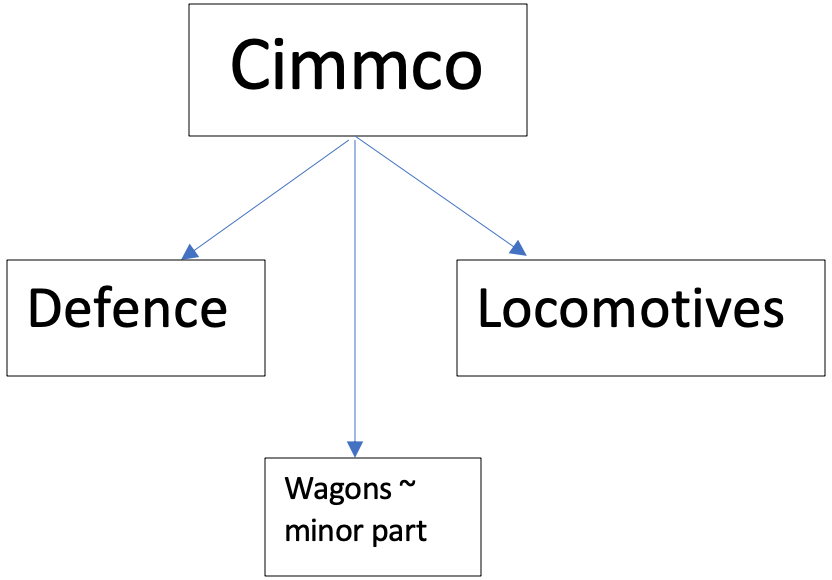

Post-merger, in the latest available conference call, the management has given the guidance that the company will move towards the business of defence products and locomotives shell. This announcement brings a change in the business dynamics of the company.

Now locomotives are like an engine, that pull/push the wagon (boxes) of a train ~ to simplify to the lowest level.

The shares will continue trading but the company will move towards a different business and we will try to gauge through management the new business the company will be in.

The exchange ratio is as explained as follows: for every 24 shares held by the investor in Cimmco, they will receive 13 shares of TWL. TCPL will be merged, with cancellation of its shares.

Umesh Chowdhary, Vice Chairperson and MD of the company, pointed out in the call that the order book for locomotive shell and cannisters for defence, is healthy. Though, the company will continue manufacturing some wagons and some specialised wagons, but primary it will be concentrating on the above mentioned products.

So, drawing for all the discussions and observation, the following flow chart shows the company’s primary business segments.

We don’t have number to gauge about the new businesses the company is in but one can look at some of the developments that has been happening recently in the defence industry.

Due to the Atmanirbhar Bharat appeal by the PM, the Ministry of Defence has banned the imports of 101 items, mainly weapons and military platforms including artillery guns, assault refiles and transport aircraft. This is done to boost indigenous production in the country.

The MoD has also announced a Rs.52000 crore domestic capital procurement plan to give an encouraging start to the domestic defence manufacturing. Rajnath Singh, Cabinet Minister of Defence expects that the domestic defence manufacturers will receive orders worth Rs.4 lac crore within the next 5-7 years.

The ministry has also started having meetings with friendly countries about their defence requirements that can be fulfilled by the Indian domestic industry.

These are positive signs for the industry.

Valuation

Looking at latest investor conference call, the management wants to reduce debt at the corporate level. The wagon as well as the locomotives industry is directly correlated with the economic scenario of the country and the GDP growth. This will be reflected in the company’s FY20 and FY21 annual reports, negatively. The wagon business will be supported by low oil prices as well as private contracts being looked at by the company. The number of wagons dispatched was disclosed by the management to the tune of 200 by the company.

According to us, the business is volatile in nature, show hints of recovery, changing its business dynamics and focusing on reducing its debt. Key risk include contingent liabilities, debt level, raw material volatility and auditor’s opinion.

For Sources Click Here

Disclaimer:

The Author(s) shall take no responsibility for any losses occurring out of investment/trading decisions you make based on the contents of this article.

We are not SEBI registered investment advisors. This article is meant for educational purposes only, please consult your investment advisor before acting upon any information you see here.

We may or may not have open positions, kindly assume that we are biased.

Follow Us @

Some Unrelated Stories!

Sources

https://www.thehindu.com/business/Industry/wagon-sector-set-for-a-shake-up/article27766620.ece

https://www.ibef.org/blogs/india-strong-in-tractor-manufacturing

http://www.tmaindia.in/tractor-industry.php

https://www.indianmirror.com/indian-industries/tractor.html

https://economictimes.indiatimes.com/cimmco-ltd/quarterly/companyid-13882.cms

{kind=link}