Let’s pin the most important factor right at the start of this section: HIGH POTENTIAL REWARD COMES WITH HIGH RISK.

So, where do I invest my savings?

In a world, where there are new investment solutions popping-up every fortnight, this sure becomes a dodgy question to answer.

A few famous investment options are:

Equity – Variable return class – relatively risky; but the upside potential is infinite

Debt – Fixed return class – relatively safe (conditions apply); but limited upside

Physical Property – Hybrid returns – Risk of high opportunity cost – Very illiquid

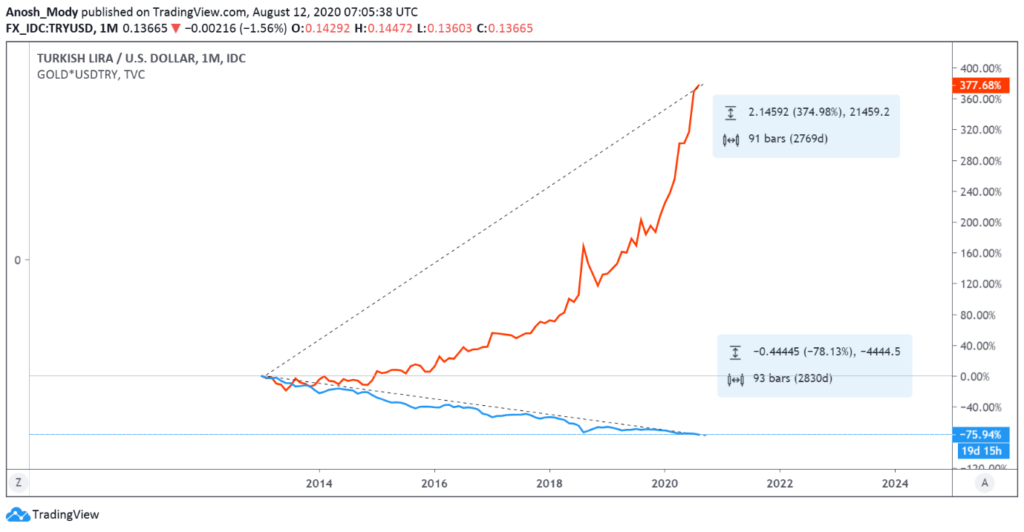

Gold – A good hedge against almost everything, including depreciation of the home currency

And a few new-age investment options like cryptocurrency, equity derivatives, hybrid insurance-investment solutions, financial instruments linked to physical property, start-up financing and many, many others!

Let’s look at each asset class in brief:

{kind=link}