In the last few weeks, IT stocks along with Private Bank stocks have been driving the market higher and higher with the SENSEX reaching the level of 40,900 on Wednesday (21st October, 2020). In the past month, NIFTY Private Bank Index has moved from 11,200 to 13,600 which can be seen as a giant leap. The change is majorly driven by Axis Bank (23%) with HDFC Bank (19%) and ICICI Bank (16.5%) in the past month. Why are more people investing in private banks?

There are a lot of reasons for the surge in the investments in the Private Sector Banks which includes lower NPAs, better asset quality and a large customer base. In 1994, private banks started emerging in India such as HDFC Bank, IndusInd Bank and ICICI Bank. Liberalization really stands out here as with strong competitors, the overall output and quality of the sector improves as everyone wants to be better and thus aims towards it. These banks offer various levels of customer relationship such as Privy League or Diamond Customer and many more such gamification ideas to provide the best service to the people.

A lot has been going on with the safety of the Public-Sector banks as well. From the Punjab National Bank (PNB) scam to the Punjab and Maharashtra bank loan fraud, there is an increase in the defaults of the government banks which can be due to the low asset quality and high NPAs. State Bank of India, which is the largest government bank has a market cap of 180k Cr which is around 1/3rd of the market cap of HDFC Bank (662k Cr).

There are around 22 private banks in India. Out of these, the major players include HDFC Bank (662k Cr), Kotak Mahindra Bank (272k Cr), ICICI Bank (287k Cr) and Axis Bank (150k Cr). Realistically, these are the best bets to make on in the private banking sector during the COVID times. Aditya Khemani, the fund manager of Motilal Oswal Securities said that:

“The top four private sector banks would be stocks I would play in the sector because these will be the survivors of a bad cycle and will make merry in the next one, two, three years as and when normalcy returns.”

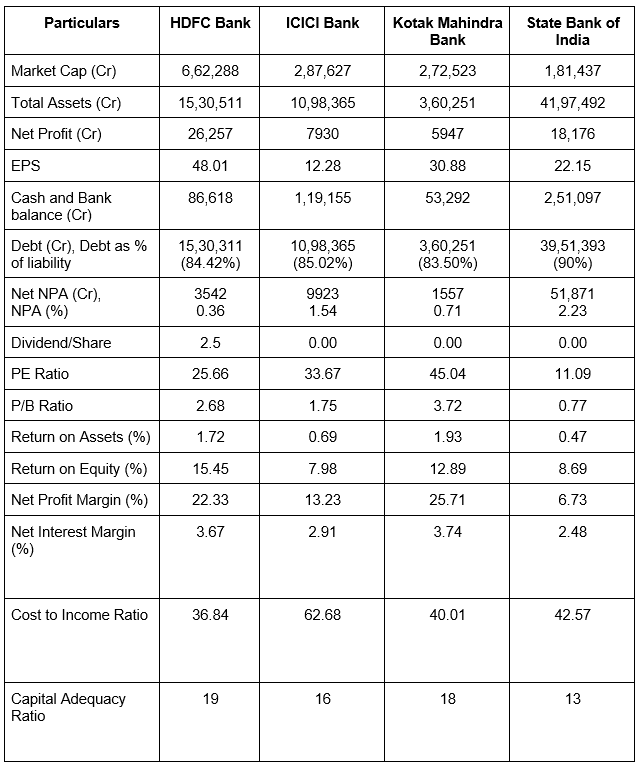

This makes sense as it is very uncertain as to when the “Old Normal” will come and the bank with a strong balance sheet will surpass and be on the top. During these tough times, people and corporations would be in need of money, so the banks who lend more would be doing good in the long run. Let us compare some of the data (2020) of the top three private sector banks to the top public sector bank which is the State Bank of India (SBI).

There are many ratios to analyze but from aforementioned ratios, we can clearly see some trends:

i. Return on Assets (RoA) should be >1% as a rule of thumb. HDFC and Kotak Bank have best-in-class RoA in comparison to SBI which has a very low RoA (0.47%). Even though SBI has total assets more than the three combined and has a larger customer base, the RoA is still very low. We can clearly see that the Non-Performing Assets (NPA) of SBI are very high which confirms the lower asset quality of SBI.

ii. The Industry PE for Private-sector banks is 29. HDFC with strong fundamentals and a low PE ratio is undervalued as of now, and it might be a good strategy to buy on dips and hold for the long term. In this sector, HDFC followed by ICICI and Kotak Bank are the hotshots and these banks are strong enough to withstand the COVID pandemic with their strong books.

iii. A good Return on Equity (RoE) for a bank is over 10% by the rule of thumb. Even here, HDFC stands out amidst the competitors as it has a staggering RoE of 15.45%. Also, no other competitor gives out Dividend, but HDFC does give a dividend of Rs 2.5/share. An added reason to make an investment!

iv. The Net Interest Margin can be found by this formula:

As a rule of thumb, the higher the better. This is a very good indicator to analyze bank stocks and here too, HDFC Bank stands out. The Net Profit Margin is also very high in the private bank sector and there is a drastic difference which is very evident here.

v. Cost to Income ratio is

A lower ratio is better as it suggests that the company is managing the costs well and using all the resources efficiently. HDFC takes the advantage here also while ICICI has a very high ratio which indicates that the company is not efficient in controlling costs.

vi. Capital Adequacy Ratio and CASA ratios are specific to banks. CAR highlights the ratio between the bank’s capital to its risk. Higher the ratio, the better it is as it can withstand financial difficulties. With the COVID pandemic, this becomes even more important and HDFC has a higher CAR ratio which strengthens its position in the sector.

There are several more ratios (Liquidity, Solvency, Valuation and Profitability) to analyze and one can always find the intrinsic value of the stocks using methods such as Discounted Cash Flow (DCF) or the EV/EBITDA method. After seeing the above table, the best private sector bank to invest in is probably HDFC Bank followed by Kotak Mahindra Bank and ICICI Bank. These are the big players in the field, but a lot of the small private sector banks have been emerging which may be a good buy for the long term. These hidden gems have not achieved their full potential and are still expanding. Some of these hidden gems are:

1) IndusInd Bank

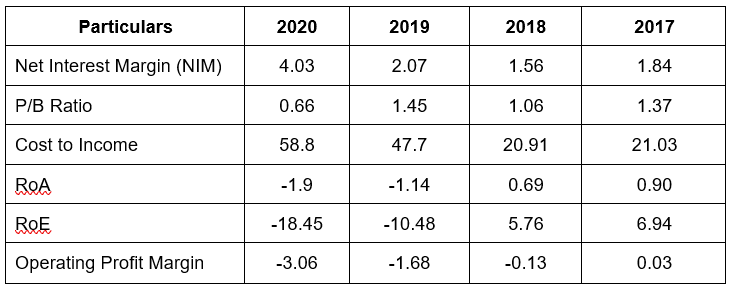

Founded in 1994, IndusInd Bank has the 6th largest market capitalization in the private bank sector of 32,370 Cr. It is definitely a very good investment right now as it fell from 1400 and is presently trading at around 600. There were many reasons as to why it fell such as: Change in the management (Ramesh Sobti retired) and the erosion of deposits by around 10%. It reached a low of 250s and is now trading at the level of 600. Let us look at some of the financials (2020) and do a comparative analysis:

Now, the financials of IndusInd Bank are not better than HDFC Bank or the other top banks. They definitely seem a bit shaky and bleak. NIM increasing is a good sign of growth of the bank while a steep dip in the P/B ratio could mean that the stock is undervalued. However, it could also mean that financial distress or a plunge in earning power. The RoA and RoE is more or less consistent throughout the years with a slight decreasing trend. The fundamentals are not the strongest but there is one thing IndusInd Bank has an edge in: Digital Banking.

IndusInd Bank witnessed a 3X increase in the digital account openings from the pre-Covid levels. With the pandemic going on, digital banking is reckoned as the “new normal”. Further, IndusInd Bank became the first bank in India to introduce an online facility for opening current accounts in a completely digitized (paperless) medium. The bank’s Chief Digital Officer highlighted that IndusInd Bank has been ahead of the curve among its peers in terms of technological innovation and has been able to invest in customer relationship management (CRM) even during the COVID-19 times. The bank has a variety of digital banking initiatives such as:

- IndusMobile:

This app helps you bank online (make transactions, check account balance, get statements and many more) along with other offers such as ordering food, paying bills or calling cabs. A lot of gamification concepts such as cashbacks and discount offers have been incorporated and people can avail the maximum from it.

- Social Media Banking:

There are provisions of banking on various platforms such as WhatsApp, Facebook and Twitter.

- IndusSmart:

Within a click, people can plan and change their investments in mutual funds, bonds or any other assets.

Another innovative product which IndusInd Bank has come up with is a Battery-powered Interactive Credit Card. Instead of a normal credit card, it consists of three actual buttons: Pay by EMI, Pay by Credit and Pay by Credit. A person can choose any option with the press of a button. Again, an element of gamification is introduced here.

For every Rs 150 spent, a customer earns 1 Reward Point. One can redeem these points on various incentives such as 1 point for 1 airline mile, movie tickets, fuel waivers and many more.

IndusInd Bank surely does not have strong financials, but they definitely have a lot of innovative products out there. They have shown a strong hold in the digital banking industry and are expanding more into the space with an increasing customer base. At the current market price of 600, it is probably undervalued and can be bought on dips.

2) IDFC First Bank

Many people have said that IDFC First Bank has the potential to be the next HDFC Bank. This bank was created by the merger of IDFC with Capital First (An American Bank). A reason why this bank started to get attention lately was due to V Vaidyanathan, who joined as the MD of the IDFC First Bank in 2018. Mr. Vaidyanathan is known for the transformation of ICICI into a Universal Bank from a Domestic Financial Institution (DFI). When ICICI Bank was formed, as the head of the Retail sector, he grew the business to 1400 branches and more than 25 million customers. The management led by the 29 years of experience of V Vaidyanathan is very strong and extremely integral. Let us look at the financials of 2020:

IDFC First Bank does not have the best fundamentals. RoA and RoE have been decreasing YoY and also the operating profit margin has been decreasing. Also, with the cost to income ratio increasing, all of these ratios give a negative impression of IDFC First Bank.

However, if one sees the quarterly results, they have been on a positive note since the past two quarters. The Net Profit for Q4 FY19 was 76 Cr and it increased to 100 Cr for Q1 FY20. Along with this, the Net NPAs also decreased from 808 to 436 (in crores) between the two quarters. We can expect better results in the upcoming quarters which would strengthen the fundamentals.

One of the most innovative things which IDFC First Bank has been associated with is: FamPay.

FamPay is a neobank offering banking services to children above 10 years of age in partnership with IDFC First Bank. FamCard is a numberless debit card launched in partnership with the IDFC First Bank which has been accepted across the RuPay payment network of merchants. The card has no numbers on it. It generates a PIN for every transaction and children can use the PIN to make offline payments. For online transactions, the app has a virtual card which has all the details such as numbers or CVV. Gamification is always present with cashbacks offered on reaching different savings milestones.

There are over 250 million+ children in the age range of 12-18 out of which over 20 million have smartphones. Traditionally, a young kid would have to ask for money from parents every time he/she wants to buy something. But with FamCard, they can make online and offline payments without making a bank account. Thus, FamPay gives financial independence to the children with a feature of control and supervision of their transactions by their parents. IDFC First Bank gets a lot out of it as their bank is the first one a kid would have been associated with. Usually, the memories and associations a person has in his/her childhood remains with him/her forever. The child would still remember the first time he made a payment using IDFC Bank which makes him/her a loyal customer in the future. Thus, with the idea of developing a dedicated and loyal customer base, IDFC First Bank would possibly grow a lot with FamPay.

V Vaidyanathan is building a fundamentally very strong bank. With the financials improving slowly with a very dedicated and strong management team, IDFC First Bank will keep on growing and growing with innovative partnerships such as FamPay. It may just become the next HDFC Bank.

There are many other Private Banks too which have been showing potential. Bandhan Bank, Ujjivan Small Finance Bank and Federal Bank are few. They have good fundamentals which seem to be increasing YoY. However, in these uncertain and riskier times, it is better to be safe and choose an investment very carefully. It is not easy to survive the economic downturn and the aftereffects of the pandemic. The one with the strongest books are the ones most likely to do so.

Disclaimer: All the opinions and interpretations are of the author.

Follow Us @

{kind=link}