Lemonade is a company that I have followed closely ever since its inception circa 2015. Now, after its big bang IPO and the nearly 150% price rise since, I feel compelled to share what I know about the company and why I am rooting for its success.

Lemonade can be best understood as a first principles organisation – one built completely from the ground up, disregarding and often contrary to traditional industry practices. Established by 2 seasoned tech professionals – Dan Schreiber & Shai Wininger, the first big thing that stands out is the fact that neither of the founders had any prior insurance experience, a rarity in an industry where the mere understanding of the business model and regulatory framework are strong barriers to entry.

Second is about how lemonade is structured. Disciples of Warren Buffet I’m sure know about the concept of the insurance float. For the uninitiated, it basically means that insurance companies, especially ones who have no responsibility to return participating interest (investment profits) to policyholders, gain tremendously from the simple fact that customers pay insurance premiums upfront, which are then invested. All the returns made on that investment are then retained by the insurance company itself.

In the words of the Oracle of Omaha himself:

Insurers receive premiums upfront and pay claims later. … This collect-now, pay-later model leaves us holding large sums — money we call “float” — that will eventually go to others. Meanwhile, we get to invest this float for Berkshire’s benefit. …

If premiums exceed the total of expenses and eventual losses, we register an underwriting profit that adds to the investment income produced from the float. This combination allows us to enjoy the use of free money — and, better yet, get paid for holding it. Alas, the hope of this happy result attracts intense competition, so vigorous in most years as to cause the P/C industry as a whole to operate at a significant underwriting loss. This loss, in effect, is what the industry pays to hold its float. Usually this cost is fairly low, but in some catastrophe-ridden years the cost from underwriting losses more than eats up the income derived from use of float.

Insurance companies survive on float and it becomes a key factor in all strategic decision making. This float, while not being a bad thing, may disincentivize traditional insurance companies from being more prudent in issuing (underwriting) insurance policies.

Further, the fact that the entire insurance premium is a windfall for the insurer creates fundamental conflicts between the insurer and the insured. Anyone who’s tried to claim an insurance payout has gone through the arduous process of long waits, frivolous rejections etc. This is because the insurance company will often try to do everything in its legal powers to not pay you, as that directly affects their bottom line (and their employees’ bonuses). This misalignment in incentives explains some of the bitter attitude the general public has to insurance.

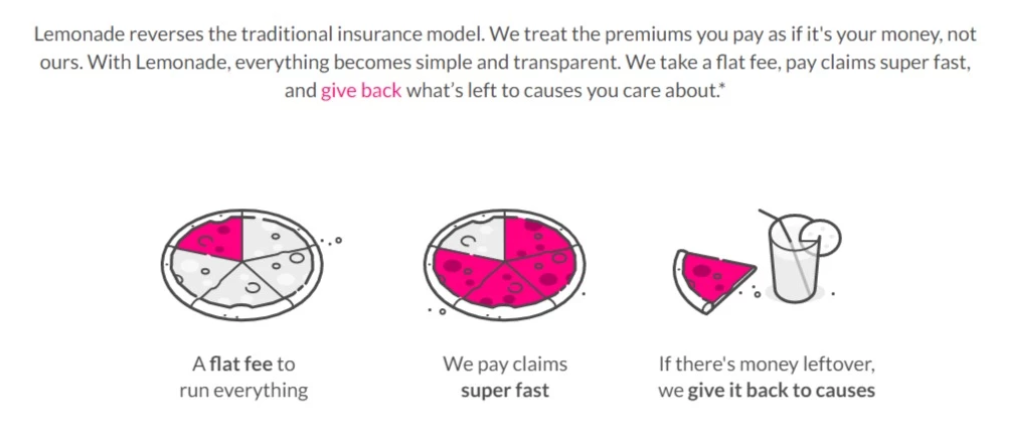

Lemonade saw this as an opportunity to build a new type of insurance company – one that did not treat customer premium like its own, but as a custodian – much like an asset manager would with money.

But before I dive down that rabbit hole, I need to explain the concept that insured risk is practically a commodity that can be bought and sold by institutions. We as consumers don’t see this side of risk as its usually reserved for large institutional markets such as Lloyd’s of London. We see it as a future liability that we want to get rid of and protect ourselves, a prudent thing to do for an individual and his family. However, risk isn’t a future liability but a contingent liability. The insurance company’s obligation does not always crystallize and the insurer pockets all the money you have given him. And more often than not, this risk is repackaged and sold to re insurers who then subsequently deal in a $300 billion risk market.

While all these insurance companies work on the model of holding and then trading risk like inventory, Lemonade on the other hand act like an agent, limiting its upside to a fee based structure (25% of premium). This ensures that that conflict between the company and the policyholder does not arise as the insurer has nothing to gain from not paying out claims, thus creating a much better experience for the customer.

How Lemonade Works

Here is another interesting part of lemonade’s business model – it isn’t a company at all, but a public benefit corporation. This is a type of hybrid entity that exists for profit, but also to ensure community driven growth and success. Lemonade organises its income as a fee of the premium, the balance of which (after allowing for actuarial liability creation) is subsequently given away to causes the organization has planned to support – such as the ACLU, UNICEF, The American Red Cross etc.

It’s mission is worded aptly – “Converting a necessary evil into a social good.”

While all this sounds great for the customer and for the community, it still does not explain what the astute money-minded investors at Softbank, Sequoia, Google and subsequently Wall Street saw in this young upstart in an industry dominated by 100-200 year old titans to give it a $2 billion valuation. This is where the tech comes in Insurtech.

Lemonade is a Property and Casualty insurer, focusing mainly on 2 products – renter’s and homeowner’s insurance. This market is dominated by 2 insurers in the US – Statefarm and Allstate. In order to justify it’s lofty valuations, Lemonade will have to go toe-to-toe with these behemoths, a lofty task. However, the founders see a massive opportunity to disrupt these bureaucratic and inertia-prone organizations by leveraging Lemonade’s 2 key advantages – distribution and technology.

The distribution part quite is simple to understand. Neo Bank (e.g. Chime) successes have validated the long held notion that millennial and Gen Z customers are not willing to settle for the same old customer experience of traditional financial services, of which Insurance has arguably the worst. Lemonade, among others, changed that by introducing speed, convenience and seamlessness in their offering. It’s on-boarding is a breeze, payouts are near instant, and the entire process is paperless. Much less intimidating than the sheets of policy documents that invoke a sense of despair in the best of us.

Another thing that lemonade does well is to not use insurance brokers. While the traditional insurance companies rely on brokers as a primary distribution channel, lemonade is not limited by these constraints as the internet is the biggest distribution channel there is for its target audience. Further, brokers charge a hefty commissions – up to 28% of net premiums. Lemonade does well by steering clear of these costs. No wonder that over 75% of Lemonade’s customers are below 35 and over 90% of them are first time insurance buyers.

Distribution helps Lemonade ensure fantastic premium growth of 200% from $22.5m to $67m in a year, but insurance companies should be wary of growth. Accounting matching says that every income has an expense. Insurance is an exception. Incomes come with the baggage of risk. Almost like a bookmaker taking bets on future events. Like with any bet, the results can be tremendous upside or catastrophic downside. Hence hedging and diversification become integral. Indiscriminate selling of poor quality homogeneous policies i.e. ones with greater than normal risk, exposes the company to potential bankruptcy in case the tide turns. Hence effective risk management and mitigation can be a major competitive advantage for an insurance firm. Lemonade has done so using techniques that were alien to the industry before they came in, mainly revolving around Artificial Intelligence.

Remember how I said Lemonade is a first principles organization? Well, the following idea drives that point home. Dan, the CEO, on Azeem Azhar’s podcast describes insurance as the original data science industry. He says that the mathematicians and statisticians who now work at Google, Apple etc. today would all have worked at insurance companies in the pre-silicon valley 20th century. This begs the question as to why isn’t the $1.3 Trillion insurance industry, one that would arguably benefit the most from cutting edge data analytics and AI, not at the forefront of this innovation? What is stopping insurance from adopting Silicon Valley’s best practices to improve its business model?

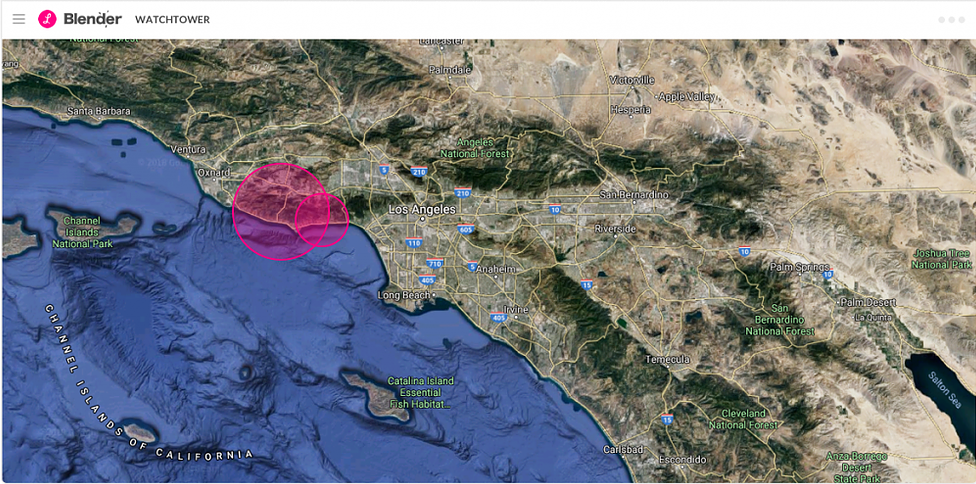

Dan and the Lemonade team have let their actions answer that question. They have introduced measures such as internal AI assistant bots (‘Cooper’) for ops automation. These bots not only support human underwriters, but in some cases underwrite policies autonomously as well. Cooper in fact, according to Dan, is an integral pillar in the organization collaboration structure. Lemonade has also introduced real-time alternate data monitoring for insurance pricing and underwriting management. The most prominent example I can give is of Watchtower – an AI layer connected to NASA’s Continental Satellites to track and predict wildfires so as to price as well as to limit issuance of Home insurance in those particular zip codes in real time.

A big synergy that insurance and AI have is scale. Insurance companies become more predictable, diversified and hence better quality businesses with scale. Similarly, AI improves accuracy as it iterates across new and more diverse test data over a period of time. Hence as the organization grows, early deployment of AI should theoretically pay handsome dividends. It has been seen in other industries, my best bet is that the same norm will continue in insurance a well.

Even with all the buzz around Lemonade though, It is important to remember that the above innovations are new and far from perfect. In fact, in their first year Lemonade faced loss ratios (Payout : Premium) of up to 166%, much higher than the industry standard of 65%, but subsequently they have come down to a more modest figure of 86%. Further, the doubling revenues as seen earlier are also accompanied with doubling losses from $52m to $108m. Lemonade also counts for less than 1% market share in P&C insurance, showing immense growth potential as well as great risks.

Despite this, with Lemonade’s listing, I feel a sense of hope for the future of insurtech. While they are the first, they are most definitely not the last in the line of large scale future-oriented insurers, built around their customers and their communities. There will be lots of missteps to come in the future as well, but it heartening to see the commitment Lemonade has to innovation and access in an industry that thrives on complexity. I root for lemonade as a someone who recognizes the power the insurance industry has to serve the world as a ‘necessary evil’, with the nudge in the right direction.

The article first appeared at Percapita.in: https://www.percapita.in/post/when-life-gives-you-lemons

Follow Us @

Subcribe to Our Mailing List!

Behavioral Aspects in Decision Making (Part 2)

{kind=link}